by David F. von Hippel and Peter Hayes

19 November 2013

This Special Report was originally published as a Working Paper 2013-1 by the Center for Energy, Governance and Security at Hanyang university, Seoul.

I. INTRODUCTION

This Special Report by David von Hippel looks at the relative impacts of different fuel cycle options on other aspect of (broadly defined) energy security.

In this Special Report von Hippel presents a summary of the current status of and recent trends in electricity consumption in general, and nuclear generation capacity in particular, in the nations of East Asia and the Pacific, offer three future scenarios of nuclear power development in the region (section 2); notes some of the options for nuclear fuel cycle cooperation that have been previously offered for the region, and describe and evaluate four potential scenarios for nuclear fuel cycle cooperation (or non-cooperation) in the region (section 3); and describes some of the key conclusions of the analysis of fuel cycle options for energy security policies in the region (section 4).

David F. von Hippel is a Nautilus Institute Senior Associate. His work with Nautilus has centered on energy and environmental issues in Asia, with a particular emphasis on Northeast Asia and North Korea.

The views expressed in this report do not necessarily reflect the official policy or position of the Nautilus Institute. Readers should note that Nautilus seeks a diversity of views and opinions on significant topics in order to identify common ground.

II. SPECIAL REPORT DAVID VON HIPPEL

Potential Regional Nuclear Energy Sector Cooperation on Enrichment and Reprocessing: Scenarios, Issues, and Energy Security Implications

Over the past two decades, economic growth in East Asia—and particularly in China, the Republic of Korea (ROK), Vietnam, Taiwan, and Indonesia—has rapidly increased regional energy requirements, especially electricity needs. Although economic growth slowed in much of the region during the global recession of 2008-2010, and electricity demand in Japan declined in the aftermath of the accident at the Fukushima reactor following the March, 2011 Sendai earthquake and Tsunami, overall growth in demand for electricity in the region continues. As a recent, eye-opening example of these increased needs, China added nearly 100 GW of generating capacity—more than the total generation capacity in the ROK as of 2010—between 2009 and 2010 alone. Despite efforts to boost hydroelectric and other renewable generation, the vast bulk of the capacity Chinas adds each year is coal-fired, underlining concerns regarding the global climate impacts of steadily increasing coal consumption.

With the lessons of the “energy crises” of the 1970s in mind, several of the countries of East Asia—starting with Japan in the mid-1970s, and continuing with the ROK, Taiwan, and, in the early 1990s, China—have sought to diversify their energy sources and bolster their energy supply security, as well as achieving other policy and social objectives, by developing nuclear power. Several other East Asian nations are currently discussing adopting nuclear power as well, if not, like Vietnam, taking concrete steps toward developing their own nuclear facilities. At the same time, global security concerns related to terrorism and to the nuclear weapons activities of the Democratic People’s Republic of Korea (DPRK), Pakistan, and India, as well as the (nominally peaceful) uranium enrichment programs pursued by Iran and, as revealed publically in 2010, the DPRK, have focused international concern on the potential for proliferation of nuclear weapons capabilities associated with nuclear power. In addition, old concerns regarding the management of nuclear spent fuel and other wastes, including the safety and long-term implications of various means of spent fuel management and/or disposal, as well as the siting of spent fuel facilities, remain, at best, only partially addressed.

One means of addressing proliferation concerns, reducing environmental and safety risks of nuclear power, and possibly of modestly reducing the costs of nuclear energy to the countries of the region, is regional cooperation on nuclear fuel activities. A number of proposals for regional cooperation on safety, enrichment, spent-fuel and waste management, and other issues have been offered over the years, some from within the region, and some from outside the region. The net impact, however, of regional nuclear cooperation on the energy security—expressed broadly to include supply security, economic impacts, environmental security, and security related to social and military risks—requires a more detailed look at how cooperation on nuclear power might be organized and operated. Working with a network of collaborating teams in nine countries of the region, Nautilus Institute has defined several different scenarios for nuclear fuel cycle cooperation in East Asia, evaluated those scenarios under different sets of assumptions regarding the development of nuclear power in the region[1]. These evaluations of the physical flows of nuclear fuel cycle materials and services, and of the costs of different elements of the fuel cycle, help to shed light on the relative readily quantifiable costs and benefits of different regional fuel cycle cooperation options. At least as important, however, are the relative impacts of different fuel cycle options on other aspect of (broadly defined) energy security, which can be evaluated qualitatively.

In the remainder of this EGS Working Paper, we:

- Present a summary of the current status of and recent trends in electricity consumption in general, and nuclear generation capacity in particular, in the nations of East Asia and the Pacific, offer three future scenarios of nuclear power development in the region (section 2);

- Note some of the options for nuclear fuel cycle cooperation that have been previously offered for the region, and describe and evaluate four potential scenarios for nuclear fuel cycle cooperation (or non-cooperation) in the region (section 3); and

- Describe some of the key conclusions of the analysis of fuel cycle options for energy security policies in the region (section 4)[2].

1 Nuclear Power and Nuclear Spent Fuel Management in the East Asia and the Pacific

East Asia and the Pacific includes three nuclear weapons states—including the United States based on its physical proximity and presence in several territories, as well as its geopolitical and cultural importance in the region—plus one (the DPRK) that is nuclear-armed since 2006. The region also includes three major economies that are nearly completely dependent on energy imports and for which nuclear energy plays a key role, a nuclear materials supplier nation currently without commercial reactors of its own, and at least two populous and fast-developing nations with stated plans to pursue nuclear energy. Table 1 provides a summary of the status of major nuclear fuel-cycle activities in each country covered by this Working Paper. To this listing can be added Mongolia, which has significant uranium resources and a history of uranium production and exploration during Soviet times. Though Mongolia has no other active commercial nuclear facilities, its involvement in regional nuclear fuel cycle activities related to uranium supply has been proposed[3]. Mongolia’s status as a nuclear weapons-free state, a process begun in 1992 and recently (2012) formalized through recognition by the five permanent members of the United Nations Security Council[4], also potentially makes it an interesting “player” in nuclear weapons policy in the region.

Table 1: Summary of Nuclear Energy Activities in East Asia/Pacific Countries

|

Country |

Nuclear Generation |

Front-end Fuel Cycle Activities |

Back-end Fuel Cycle Activities |

| Japan | Mature nuclear industry (~47 GWe as of 2010) with continuing slow growth until Fukushima accident. Post-Fukushima 4 units closed, all other power reactors in Japan shut down for inspection as of late May, 2012[5]; some since restarted. | No significant mining, milling. Some domestic enrichment, but most enrichment services imported. | Significant experience with reprocessing, including commercial-scale domestic facility now in testing (though much delayed), plus significant reprocessing in Europe; interim spent-fuel storage facility in use. |

| ROK | Mature nuclear industry, 23 units totaling 20.8 GWe at 4 sites as of late 2012[6]. | No significant uranium (U) resources, enrichment services imported, but all fuel fabrication done domestically. | No reprocessing, but “pyroprocessing” under consideration; at-reactor spent fuel storage thus far. |

| DPRK | Had small (5 MWe equivalent) reactor for heat and plutonium (Pu) production, now partly decommissioned; policy to acquire LWRs, and currently building LWR with domestic technology estimated at 100 MWth[7]. | At least modest Uranium resources and history of U mining; some production exported; operating 2000-centrifuge enrichment plant recently revealed[8] (Hecker, 2010) | Reprocessing of spent fuel from 5 MWe reactor to separate Pu for weapons use. Arrangements/plans for spent fuel management for new reactor unknown. |

| China | Relatively new but rapidly-growing nuclear power industry; 14.2 GWe in 20 units as of 2012. | Domestic enrichment and U mining/milling, but not sufficient for large reactor fleet. | Nuclear weapons state. Small reprocessing facility; plans underway for spent fuel storage facilities. |

| Russian Far East (RFE) | One small plant (48 MWe) in far North of RFE (Russia itself has a large reactor fleet); plans for larger (1 GWe scale) units for power export. | Domestic enrichment and U mining/milling (but not in the RFE). | Nuclear weapons state. Russia has reprocessing facilities, spent fuel storage facilities (but not in RFE). |

| Australia | No existing reactors above research scale; has had plans to build power reactors, but currently very uncertain. | Significant U mining/milling capacity, major U exporter (over 6000 t U in 2011[9]); no enrichment. | No back-end facilities. |

| Taiwan | ~5 GWe in 6 reactors at 3 sites, 2 additional units at 4th site under construction since late 1990s, but their completion is under review post-Fukushima, with conversion to gas being investigated[10]. | No U resources, no enrichment—imports enrichment services. | Current spent-fuel storage at reactor, no reprocessing. Siting of low-level waste and intermediate spent fuel storage under discussion. |

| Indonesia | No current commercial reactors, but full-scale reactors planned. | Some U resources, but no production; no enrichment. | Consideration of back-end facilities in early stages. |

| Vietnam | No current commercial reactors, but a number of full-scale reactors planned, with agreements signed recently with Russia, Japan, ROK for reactor construction and finance[11]. | Some U resources, but no production; no enrichment. | Consideration of back-end facilities in early stages. |

1.1 Current Status of Electricity Consumption and Nuclear Generation

Recent growth in electricity generation and use in East Asia has been remarkable. As an example, Figure 1 shows total electricity generation in the Northeast Asia region more than tripled between 1990 and 2011, with generation in China increasing by nearly a factor of eight, generation in Taiwan increasing by a factor of nearly three, and generation in the ROK increasing by a factor of 4.4. Even though electricity production in Japan—which in 1990 had the highest generation in the region—grew by only 31 percent (an average of 1.3 percent annually), the fraction of global generation accounted for by the Northeast Asia region grew from just over 15 percent in 1990 to over 30 percent in 2011, even as electricity generation in the rest of the world grew at an average rate of 2.0 percent annually.

Figure 1: Electricity Generation in Northeast Asia, 1990-2011

![Sources: Data from British Petroleum “Statistical Review of World Energy 2011” workbook[12] for all countries except the DPRK (based on updated Nautilus Institute results not yet published[13]), Mongolia (based on data from USDOE/EIA[14]), and RFE (estimated from paper by Gulidov and Ognev[15]). Generation figures shown are for gross generation (that is, including in-plant electricity use), except for Mongolia and the RFE.](https://nautilus.org/wp-content/uploads/2013/11/firgure-1.png)

Sources: Data from British Petroleum “Statistical Review of World Energy 2011” workbook[12] for all countries except the DPRK (based on updated Nautilus Institute results not yet published[13]), Mongolia (based on data from USDOE/EIA[14]), and RFE (estimated from paper by Gulidov and Ognev[15]). Generation figures shown are for gross generation (that is, including in-plant electricity use), except for Mongolia and the RFE.

Against this backdrop of growth in electricity needs—existing “business as usual” projections call for continuing strong increases in electricity use in the countries of East Asia (with the possible exception of Japan)—many of the countries of the region face significant energy resource constraints. The industrialized economies of Taiwan, the ROK, and Japan import over 90 percent of their energy needs. Vietnam and Indonesia, though they have been net energy exporters for several decades, are at or near the point where they will become net importers. China, though endowed with large reserves of coal and significant oil and gas reserves, is obliged to meet the energy needs of an increasingly affluent 1.3 billion people, and the economy that sustains them. As a result, China is increasingly an energy importer as well. The sparsely settled Russian Far East has a vast resource endowment—including hydraulic energy, coal, oil, and natural gas—that could potentially be harnessed for export to its neighbors. A combination of severe climatic conditions, politics, and huge financial requirements for the infrastructure needed to accomplish oil, gas, and power exports have slowed development of these resource sharing schemes. Even massive international pipelines and powerlines, however, will only make a modest contribution to the energy needs of Russia’s energy-hungry neighbors[16] (see von Hippel and Hayes, 2008b).

The resource constraints faced by most of the nations of the region, together with the technical allure of nuclear power, have made East Asia a world center for nuclear energy development, and—news reports of a global nuclear renaissance notwithstanding—one of the few areas of the world where significant numbers of nuclear power plants are being added. Nations have chosen nuclear power because they wish to diversify their energy portfolios away from fossil fuels (especially oil) and thus improve their energy supply security, because nuclear power provides a stable sources of baseload power with low air pollutant emissions (particularly compared with coal), and for the less practical but still significant reason that being a member of the nuclear energy “club” is seen as offering a certain level of status in the international community.

1.2 Future Scenarios

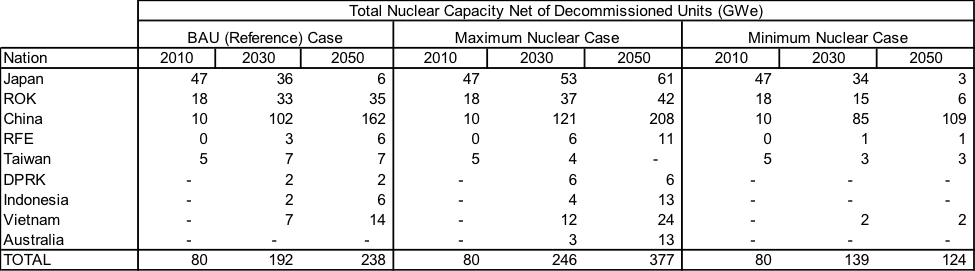

Tables 2 and 3 summarize the nuclear capacity included for each the three nuclear capacity expansion paths (Business as Usual, Maximum Nuclear, and Minimum Nuclear) for each country for the years 2010, 2030, and 2050. Figure 2 shows the capacity trend by year and country for the Business as Usual path. Key assumptions and results by country are as follows:

- Japan, with relatively little additional space for reactors and a declining population, would likely have shown at most slow growth in reactor capacity from 2010 to 2050 in a Business as Usual (BAU) case had the Fukushima accident not occurred. Given the impacts of Fukushima, however, we assume that a variant, adjusted to reflect post-Fukushima events, of was the BAU case in an earlier version of this analysis now represents the “MAX” (maximum reasonable) deployment of nuclear power in Japan, which we assume would involve the addition of about 37 percent more capacity over 38 years, mostly through the replacement of existing units (except Fukushima units 1 through 4). Our new BAU case, factoring in the physical and (more importantly) policy impacts of the Fukushima accident, assumes that all existing Japanese reactors except the damaged Fukushima units are brought back on line by 2016, with the nearly-completed Shimane-3 unit and the 40-percent-complete (reportedly, as of late 2012) Ohma-1 unit ultimately completed in 2015 and 2017, but that all reactors are phased out and not replaced by the ends of what are assumed to be 50-year operating lifetimes. This case therefore represents a significant departure for Japan, reducing its nuclear fleet to a handful of units by 2050. Our post-Fukushima “MIN” (minimum reasonable) nuclear energy case for Japan assumes that only the equivalent of about half of Japan’s existing fleet of reactors (less the Fukushima units) are brought back on line by 2016[17], that the Shimane-3 and Ohama-1 reactors are NOT completed, and, as in the BAU case, nuclear capacity is decommissioned (or placed in long-term stasis) as each unit reaches the end of its original operating lifetime, resulting in a near phase-out of nuclear power by 2050, but from a lower base than in the BAU case. We should emphasize that we anticipate that these rough revised scenarios for nuclear power in Japan will, over the next year or so, be further revised by Japanese colleagues working with Nautilus on our regional “Resilience and Security of Spent Fuel in East Asia” Project[18].

- In the ROK, the energy policy impacts of the Fukushima accident have, not surprisingly, been less marked than in Japan, but as of this writing, discussions are underway regarding the future of the ROK’s nuclear energy program[19], and will doubtless intensify as the transition to the newly-elected Park Geun-hye administration continues. As in Japan, additional reactor space is the ROK is limited, but more and larger reactors are added to existing sites in the BAU case, though at a slightly reduced rate relative to recent plans (factoring in probable delays due to policy reviews) resulting in a near-doubling of 2012 capacity by 2050. In the MAX case, where capacity increases by a factor of nearly 2.5 (though new sites would probably be needed in the MAX case). In the MIN case, existing reactors are retired without life extension and not replaced, resulting in a reduction in capacity of nearly 70% by 2050 relative to existing capacity at the end of 2012.

- For China, all three capacity expansion paths show explosive growth in nuclear capacity through 2035. Our scenarios for growth in nuclear capacity through uses as targets the “high” and “low” cases presented by Liu Xuegang[20] for nuclear capacity expansion in China through 2035. We use Prof. Liu’s high case projections as rough targets for the “MAX” path, and use his low case to set the “MIN” path, with the BAU path roughly in between. In each case, the roster of under-construction and planned plants in China presented by the World Nuclear Association[21] is adapted to fit Prof. Liu’s scenarios. Growth is assumed to continue in the BAU path after 2035, though at a lower rate as the Chinese economy matures and population begins to decline. In the MAX path, the growth rate of nuclear capacity also declines somewhat after 2030, but nearly 90 GW are still added in between 2030 and 2050, somewhat more than is added in the BAU case, but the MAX case also assumes 50-year reactor lifetimes, rather than the 40-year lifetimes assumed in the BAU case, and as a consequence total capacity grows that much more rapidly, post-2035, than in the BAU case. In the MIN case, capacity additions fall to only 1000 MW per year after 2035 (and growth to 2035 is less than in the other paths), with older reactors retired as they reach the ends of their 40-year operating lifetimes. The MIN case might be interpreted as one where breakthroughs in energy efficiency and/or renewable energy are achieved, where emerging nuclear safety, power plant siting, or other concerns, or a combination of factors slow the growth of nuclear power in China.

- The Russian Far East add some capacity between about 2020 and 2050 in the BAU case to its very small existing reactors in the far north. This capacity is mostly to serve export markets and/or to provide power for producing export commodities such as aluminum. In the MAX case, future capacity is approximately twice that in the BAU case, reflecting a stronger market for RFE power and/or minerals exports. In the MIN case, only one new (larger) reactor is added in the RFE by 2030, and no more thereafter.

- In Taiwan, as in Japan and the ROK, limited space for new reactors and a declining population limit the extent to which nuclear capacity can increase. In the BAU case, capacity increases by 2 GW, as a result of finally completing the reactors now under construction, but remains at the resulting 7 GW level through 2050. In the MAX case, larger reactors are added at existing sites when older reactors are decommissioned, pushing capacity to nearly 11 GW by 2050. In the MIN case, older reactors are not replaced, and the reactors now under construction are not completed, resulting in Taiwan’s nuclear generation capacity falling to zero by 2036.

- In the BAU case, the DPRK is assumed to reach an agreement with other parties regarding its nuclear weapons program in the next few years. In the BAU case, the DPRK completes its currently under-construction 100 MW LWR at the Yongbyon nuclear site in 2017, and operates the unit successfully, albeit at a relatively low 60 percent capacity factor. A combination of economic changes in the DPRK and warming relations with the ROK allows the completion, in a collaborative effort by the two Koreas, of the two 1050 MW reactors at the Kumho site on the East coast of the DPRK, for which construction was started in the 1990s under the Korean Peninsula Energy Development Organization (KEDO). These reactors are assumed to be completed in 2021 and 2025, respectively. Depending on the status of the DPRK electricity grid in the years before the reactors come on line, these reactors may be connected directly to the ROK grid, or possibly to a unified ROK/DPRK grid. In the MAX case for the DPRK, rapprochement between the Koreas occurs more quickly, and as a result, the DPRK abandons its construction of its small domestic LWR, and the Kumho reactors are completed sooner than the BAU case, in 2020 and 2022, followed by three more larger (1400 MW) units, possibly on a West Coast site, between 2026 and 2030. The DPRK MAX case is likely to occur only in concert with something like an ROK MAX nuclear capacity expansion case. In the MIN case for the DPRK, no reactors are built on DPRK territory through 2050.

- For Indonesia, Vietnam, and Australia, which do not have and are not yet building nuclear power capacity, the BAU case includes first reactors that come on line between 2020 and 2030 in Vietnam and Indonesia, with Vietnam’s program being much more aggressive than in the other two nations[22]. The MAX path includes greater use of nuclear power for each nation by both 2030 and 2050. Australia is assumed not to adopt nuclear power in the BAU path. In the MIN path only Vietnam adopts nuclear power, but builds only its first two reactors, which come on line several years later than expected. Neither Indonesia nor Australia ultimately adopts nuclear power in the MIN path.

Table 2: Regional Nuclear Generation Capacity, Summary of BAU, MAX, and MIN Paths

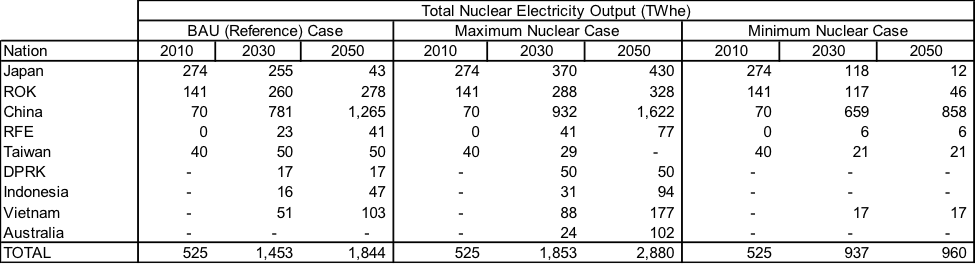

Table 3: Regional Nuclear Electricity Output, Summary of BAU, MAX, and MIN Paths

Figure 2: Trends in Regional Nuclear Generation Capacity, BAU Path

2 Regional Nuclear Cooperation Scenarios

Cooperation on nuclear fuel cycle activities could take place between all of the countries of East Asia and the Pacific, or a narrower group of several countries within the region, or a broader group of countries that could include nations outside the region. At their least demanding (in terms of costs and institutional arrangements between nations), cooperation options can involve relatively modest types of activities such as straightforward scientific, educational, and technical exchanges, or collaborations—for example, through the International Atomic Energy Agency (IAEA) or other international agencies—on sharing of information on nuclear “best practices”. More complex options include consortiums for purchasing of raw uranium or of enriched fuel. More complex still are arrangements to share enrichment and spent-fuel management facilities. An IAEA Expert Group in 2005 produced a generic review of multilateral approaches to the nuclear fuel cycle, and some of that group’s observations and suggestions are reflected in the proposals by other groups summarized below, as well as in the regional cooperation scenarios elaborated and evaluated in this paper[23]. A few of the benefits—and challenges—of regional cooperation on nuclear fuel cycle issues are listed below[24].

Potential Benefits and Challenges of Cooperation

Some of the benefits of cooperation on nuclear fuel cycle issues could include:

- Scientific, educational, and technical exchanges on nuclear fuel cycle issues help to assure that countries have a common understanding and knowledge base with regard to fuel cycle issues.

- Sharing nuclear facilities, whether enrichment, reprocessing, or spent-fuel facilities, provides viable alternative for countries that may, due to political, social, geological, or other concerns, have few positive prospects for domestic siting of such facilities.

- Achieving economies-of-scale for enrichment facilities, reprocessing centers, or geologic repositories, though economies of scale likely are stronger for some types of facilities—such as enrichment plants or mined geologic repositories—than for others, such as spent-fuel storage based on dry-cask technologies[25] (Bunn and et al., 2001).

- Creating a new revenue source for a host country.

- Sharing nuclear facilities may help to assure that all countries maintain consistent practices and quality control standards in working with nuclear materials, as well as consistent levels of safeguards, monitoring, and verification in nuclear fuel cycle activities, helping to build confidence between nations.

- Sharing of spent-fuel and reprocessing facilities can help to reduce proliferation risks by avoiding unnecessary accumulation of separated plutonium.

Implementing regional or international facilities, including those for spent fuel/radioactive waste storage/disposal, also will likely involve overcoming obstacles such as:

- Ethical issues in the region. There is some public perception that countries that have the benefits of nuclear power generation should bear the burden of storing and disposing of their radioactive wastes. This argument raises ethical and fairness issues that would oppose the concept of a regional/international repository. To obtain public and political support, an arrangement for the regional/international repository should be based on a fair and equitable sharing of benefits between a repository host and other participating countries.

- Complicating national policies in the management of spent fuel and high-level waste (HLW). A regional/international repository could distract national spent fuel and radioactive waste management programs with hopes for an international facility.

- Increasing transportation requirements in the region. The regional/international repository will involve frequent transportation of spent fuel/radioactive waste from participating countries to a host country, and increasing concern over nuclear accidents during the transportation that may lead radioactive release to the environment. Proliferation risks due to diversion of materials during transport are also a concern.

Regional (East Asia), and indeed, global nuclear fuel cycle cooperation proposals have been offered by a number of groups and individuals over the past two decades and earlier. Below we provide brief descriptions of selected prior proposals. Other authors have reviewed these and other proposals in greater detail than is possible here[26].

Interest in regional/international spent fuel/radioactive waste storage/disposal increased significantly in the 1970s and early 1980s. In 1977, the IAEA reported that regional fuel cycle centers were feasible and would offer considerable nonproliferation and economic advantages. In 1982, the IAEA concluded a project of the International Fuel Cycle Evaluation (INFCE) in which IAEA expert groups suggested an establishment of international plutonium storage and international spent fuel management[27].

In the mid-1990s, the concept of the International Monitored Retrievable Storage System (IMRSS) was proposed by Wolf Hafele. The IMRSS envisioned international sites where spent fuel, and possibly also excess separated plutonium, could be stored under monitoring for an extended period but could be retrieved at any time for peaceful use or disposal[28].

In the mid-1990s through the late 1990s, a number of proposals for nuclear power sector cooperation in the Asia-Pacific region, on topics ranging from safety to proliferation to waste management, were developed. Tatsujiro Suzuki[29] prepared a comparison of various proposals for regional nuclear cooperation offered during the period, and concluded that there are potential areas of cooperation where common needs and interests exist among the countries of Northeast Asia. At present, however, none of these proposals have been implemented to a significant degree.

The past decade has seen a number of additional proposals for cooperation on uranium enrichment, management of nuclear spent fuels, or both, many involving East Asian and Pacific countries. Brief summarizes of just some of the cooperation proposals on international enrichment and/or low-enriched uranium (LEU) fuel supply and spent fuel management that have come forth in the last 10 years or so follow[30].

The Global Nuclear Energy Partnership (GNEP), proposed by the United States during the George W. Bush administration (in 2006), had as its enrichment component a proposal to establish a group of enriched fuel supplier states, and a requirement that those states provide enriched fuel to non-supplier nations at a reasonable cost, while reducing the potential for proliferation of sensitive technologies, in part through cooperation with the IAEA on nuclear safeguards[31]. GNEP proposed coupling these fuel supply guarantees and with spent fuel “take back” arrangements. GNEP has received when the U.S. Congress cut funding to the program in 2008, and eliminated funding (except for a parallel but related “Advanced Fuel Cycle Initiative” that funds reprocessing research and development) for 2009. GNEP has, however, been recast as the International Framework for Nuclear Energy Cooperation (IFNEC), which “is a partnership of countries aiming to ensure that new nuclear in initiatives meet the highest standards of safety, security and non‐proliferation” and “involves both political and technological initiatives, and extends to financing and infrastructure” [32].

The International Uranium Enrichment Center (IUEC) and LEU Nuclear Fuel Bank, was proposed by Russia in 2006, and initiated by Russia shortly thereafter. The concept is for Russia to host the IUEC at its existing Angarsk Electrolytic Chemical Combine[33]. Membership in the enrichment center, intended to be on an “equal and non-discriminatory basis”, requires charter states to forego developing their own enrichment facilities, and be in compliance with their nonproliferation obligations (including membership in the Treaty on the Non-Proliferation of Nuclear Weapons). Reserves of LEU were placed at Angarsk in late 2010, and the IUEC Agreement went into force in early 2011, after which “the LEU reserve in Angarsk has been available for IAEA Member States”, constituting “the first proposals on nuclear fuel supply assurances to have been put into practice”[34].

In 2006, NTI (the Nuclear Threat Initiative) pledged $50 million toward an International Fuel Bank to be run by the IAEA. Since then, $100 million in matching contributions have been pledged by other countries. Similar to the Russian proposal, but not affiliated with a specific enrichment center, the goal of the Fuel Bank concept by NTI “…is to help make fuel supplies from the international market more secure by offering customer states, that are in full compliance with their nonproliferation obligations, reliable access to a nuclear fuel reserve under impartial IAEA control should their supply arrangements be disrupted. In so doing, it is hoped that a state’s sovereign choice to rely on this market will be made more secure”[35]. As of early 2010, the IAEA was planning to site the LEU repository at a remote site in Kazakhstan, at a metallurgical factory with existing storage infrastructure. IAEA member states voted in favor of the fuel bank in late 2010[36].

In April of 2007, Germany proposed to the IAEA the creation of a multilateral enrichment facility, established by a group of interested states, to be placed in a host states but on an “extraterritorial basis”[37]. Like the Russian proposal, and similar to the Fuel Bank NTI proposal, the facility would help assure supplies of enriched fuels to nations that qualify based on adherence to their non-proliferation treaty commitments and related IAEA safeguards[38].

The so-called “Six-Country” Proposal of a Nuclear Fuel Assurance Backup System, offered in 2006 by the enriched fuel supplier nations France, Germany, the Netherlands, Russia, the United Kingdom, and the United States, proposed that enrichment suppliers would substitute enrichment services for each other to cover supply disruptions for enriched fuel consumers that have “chosen to obtain suppliers on the international market and not to pursue sensitive fuel cycle activities”. Further, the proposal would provide “physical or virtual” reserves of LEU fuel for use in the event that other fuel assurances fail[39].

Also in 2006, Japan proposed an IAEA Standby Arrangements System for the Assurance of Nuclear Fuel Supply. This system would be managed by the IAEA and would offer information, provided voluntarily by nuclear fuel supplier countries, on the status of uranium ore, reserves, conversion, enrichment, and fuel fabrication in each country. The goal of this system is to help prevent disruption in international fuel supplies by acting as a kind of “early warning” system of impending supplier shortfalls for states purchasing fuel or fuel services. If a disruption in supply takes place, under this system, the IAEA acts as intermediary in helping a consumer country find a new supplier country[40].

In the 1990s, a commercial group called Pangea was looking for an international geologic repository for both spent fuel and radioactive wastes. Envisioning a facility for disposing of 75,000 MT heavy metal of spent fuel/HLW, Pangea initially selected Australia for its proposed repository, but is seeking other sites around the world after confronting political opposition in Australia[41].

During the late 1990s to early 2000s, two proposals involving depository sites in Russia were presented. One was a concept of the Nonproliferation Trust (NPT) that called for establishing a dry cask storage facility in Russia that would accept 10,000 MT heavy metal of spent fuel from abroad, and would include eventual spent fuel disposal. The other was a concept offered by MINATOM (Ministry for Atomic Energy of Russia ) that suggested a plan for an international spent fuel service involving offering temporary storage with later return of the spent fuel, or reprocessing of spent fuel without return of plutonium or radioactive wastes for customer countries[42].

In 2003, Dr. Mohamed El Baradei suggested multinational approaches to the management and disposal of spent fuel and radioactive waste[43]. In 2005, commissioned at Dr. M. El Baradei’s suggestion in 2003, the IAEA published a report on Multilateral Approaches to the Nuclear Fuel Cycle in which the IAEA concluded that such approaches are needed and worth pursuing, on both security and economic grounds[44].

In January 2006, Russian President Vladimir Putin announced a Global Nuclear Power Infrastructure (GNPI) initiative to provide the benefits of nuclear energy to all interested countries in strict compliance with nonproliferation requirements, through a network of international nuclear fuel cycle centers (INFCC). INFCC are conceived as being related to the provision of enrichment services and to spent fuel management issues through the provision of reprocessing and the disposal of residual waste within the framework of INFCC, under IAEA safeguards[45].

In 2008, Tatsujiro Suzuki and Tadahiro Katsuta proposed the idea of an “International Nuclear Fuel Management Association (INFA)” as a multilateral nuclear fuel cycle approach[46]. The central principles of the INFA are universality, meaning avoiding discrimination between nuclear “haves” and “have nots”, transparency, meaning that the IAEA “Additional Protocol” or equivalent safeguards arrangements should be applied for all facilities, and demand should come first before supply, and economic viability, meaning that the activities of the Association should be consistent with global nuclear fuel market activities, and that the economic rationale of the Association should be clearly defined to support nuclear fuel cycle programs.

2.1 Scenarios for Nuclear Fuel Cycle Cooperation in Northeast Asia

This Working Paper updates earlier Nautilus analyses of four cooperation “scenarios” for nuclear fuel enrichment and for spent fuel management. These generic scenarios borrow many concepts from the enrichment and spent-fuel management cooperation proposals summarized above. Each scenario includes specific assumptions by country for each of several fuel-cycle “nodes”: uranium mining and milling, uranium transport, uranium conversion and enrichment, fuel fabrication, transportation of fresh reactor fuel, electricity generation, spent fuel management (including reprocessing), spent fuel transport, and permanent disposal of nuclear wastes. Key attributes of the scenarios are as follows:

- “National Enrichment, National Reprocessing”: In this scenario the major current nuclear energy users in East Asia (Japan, China, and the ROK) each pursue their own enrichment and reprocessing programs, with all required enrichment in those countries accomplished domestically by 2025 or 2030. Other countries may also pursue domestic enrichment, though this scenario assumes that other countries import enrichment services through 2050. Reprocessing, using 80, 60, and 50 percent of spent fuel (SF) in Japan, the ROK, and China, respectively, is in place in Japan by 2020, and in ROK/China by 2030 Nuclear fuel is assumed to be fabricated where uranium is enriched and/or fuel is reprocessed. Half of the reactors in Japan, China, and ROK eventually use 20% mixed oxide fuel (fuel including mixed uranium and plutonium oxides, or MOx), but MOx use starts earlier in Japan than in the other nations. Japan and the ROK import uranium; other nations in the region eventually produce half of their U needs domestically except Australia, which produces all of its needs, and the Russian Far East, which imports all of its modest needs from elsewhere in Russia. Arrangements for disposal of high-level nuclear wastes from reprocessing would be up to each individual country, with attendant political and social issues in each nation. Security would be up to the individual country, and as a result, transparency in the actions of each country is not a given. Disposal of spent fuel and of high-level nuclear wastes from reprocessing is assumed to be carried out in each individual country, with interim storage or dry cask storage use assumed through 2050.

- “Regional Center(s)”: This scenario features the use of one or more regional centers for enrichment and reprocessing/waste management, drawn upon and shared by all of the nuclear energy users of the region. We avoid identifying particular country hosts for the facilities, but China and Russia are obvious candidates, though the potential involvement of other countries, including Mongolia, has been suggested. The centers are assumed to be operated by an international consortium, and drawn upon and shared by all nuclear energy users in region. The consortium imports uranium for enrichment from the international market, and shares costs between participants. China limits its own production of uranium to current levels. Nuclear fuel (including MOx) is fabricated at the regional center(s), with use of MOx by country the same as in Scenario 1. Reprocessing of spent fuel from Japan, the ROK, and China also occurs in the same amounts as in Scenario 1, but is accomplished in regional center(s) by 2025, with reprocessing of half of the spent fuel from other nations by 2050. Disposal of spent fuel and high-level nuclear wastes from reprocessing is done in coordinated regional interim storage facilities, pending development of permanent regional storage in the post-2050 period.

- “Fuel Stockpile/Market Reprocessing”: Here, the countries of the region purchase natural and enriched uranium internationally, but cooperate to create a fuel stockpile (the equivalent of one year’s consumption of natural uranium and enriched fuel) that the nations of the region can draw upon under specified market conditions. Enrichment is purchased from international sources except for the existing (as of 2010) modest Japanese and Chinese capacity. Reprocessing services are purchased from international sources, such as France’s AREVA or from Russia, while some spent fuel continues to be stored in nations where nuclear generation is used. Nuclear fuel (excluding MOx) is fabricated where uranium is enriched. Reprocessing of spent fuel is done in the same amounts as in Scenario 2, but is carried out at international center(s), where MOx fuel is fabricated for use in the region (with MOx use is as in Scenarios 1 and 2). Management of spent fuel and high-level nuclear wastes from reprocessing is accomplished using international interim storage facilities, possibly including facilities in the region, pending development of permanent regional storage post-2050.

- “Market Enrichment/Dry Cask Storage”: In this scenario, countries in the region (with the possible exception of China) would continue to purchase enrichment services from international suppliers such as URENCO in Europe, the USEC in North America, and Russia except that existing Chinese capacity enrichment capacity would continue to be used, and existing Japanese capacity would be used until it is closed after 2020. Uranium and enrichment services purchases would be through an international consortium, as in scenarios 2 and 3. Japan and China cease reprocessing in 2015, and no other countries reprocess spent fuel after that point either at international or in-region facilities. Japan’s MOx use would be phased out by 2013 and no MOx use would occur elsewhere in the region. All spent fuel, after cooling in ponds at reactor sites, would be put into dry cask storage either at reactor sites or at intermediate storage facilities. High-level wastes from reprocessing (before 2016) would also be placed in interim storage facilities.

These scenarios are not by any means intended to exhaust the universe of possible nuclear fuel cycle cooperation (or non-cooperation) options for the region, but do, we believe, represent a reasonable range of the different options that might be adopted.

2.2 Key Analytical Approaches and Assumptions

In order to the estimate the relative costs and benefits of the four nuclear fuel cycle cooperation scenarios summarized above, the following analytical approach was taken. What is presented here is necessarily a condensed description of the methods and data used; please see our more detailed 2010 report[47] for further details.

As a first step, nuclear paths specified by EASS country working groups, in some cases modified as noted above by the authors, served as the basis for calculating nuclear fuel requirements, and spent fuel arisings (including arisings from decommissioned plants). To these estimates of fuel requirements, calculated for each of the three nuclear “paths” in each country, as presented above, we overlaid the four scenarios of regional cooperation on nuclear fuel cycle issues over a timeline of 2000 through 2050. Simple stock and flow accounting was used to generate estimates of major required inputs to and outputs of the nuclear reactor fleet in each country, and of other nuclear facilities such as enrichment and reprocessing facilities. The fuel cycle nodes modeled were uranium mining and milling, uranium transportation and enrichment, fuel fabrication and reactor fuel transport, and reprocessing and spent fuel management. Key inputs at each (applicable) node included the mass of uranium (in various forms) and plutonium, energy, enrichment services, transport services, and money, accounted for by country and by year. Key outputs at each node included uranium and plutonium, spent UOx (uranium oxide) and MOx fuel, and major radioactive waste products, again by country and year. Costs are presented and calculated in approximately 2009 dollars, except where noted.

Using this approach, quantitative results for 12 different regional cooperation scenario and nuclear power development path combinations were generated. These quantitative results were coupled with qualitative considerations to provide a side-by-side comparison of the energy security—broadly defined to include not just energy supply and price security, but technological, economic, environmental, social/cultural, and military security aspects as well[48]— attributes of four cooperation scenarios. As such, we used the energy security comparison methodology developed by Nautilus Institute and its partners under a series of initiatives starting in 1998.

Many of the parameters incorporated in the analysis described here are uncertain, with the future costs of nuclear materials and facilities perhaps the most uncertain. As such, numerous assumptions informed by a variety of literature sources were used in this analysis. Some of the key assumptions used in the analysis are as follows:

- Uranium Cost/Price: $126/kg in 2012[49], escalating at 1%/yr. Uranium prices “spiked” in 2007 at over $260/kg, fell to about the $120/kg level by 2009-2010, rose again in early 2011, then began to fall, particularly after the Fukushima accident, declining more slowly over 2012 to about $120 by the end of 2012.

- Average uranium (U) concentration in ore purchased from international market sources: 2.5%: Note that this estimated average, based mostly on 2011 output data, is heavily influenced by the uranium concentration of a single highly productive mine in Canada with an ore concentration of on the order of 20 percent. Excluding this mine, the global average U concentration in ore is about 0.1%, though in practice uranium concentrations in ore vary widely[50].

- Enriched uranium from the international market is produced 30 percent by in gaseous diffusion plants in 2007, with the remainder in centrifuge-based plants, with all enrichment sourced from centrifuge-based plants by 2030 as gaseous diffusion capacity, mostly in the United States, is retired.

- Enrichment costs have fallen by nearly a quarter in the last three years, from about $160/kg per separative work unit (SWU) in 2008 through early 2010 to about $120 per kg in late 2012, likely as a result of the combination of the global economic recession and the impacts on the nuclear industry of the Fukushima accident. We assume, for the BAU nuclear generation capacity expansion case, that costs per SWU rise at 1 percent annually in real terms from 2012 level, meaning that real 2050 costs per SWU will be slightly higher than they were at the cost peak in 2008/2009. Since the MAX nuclear capacity expansion case results in higher demand for SWU, we assume that the costs per SWU will rise faster than for BAU capacity expansion, at an average rate of 2.5 percent annually. Conversely, a low rate of nuclear generation capacity expansion reduces SWU demand, so we assume no real escalation of costs per SWU is associated with scenarios in based on the MIN capacity expansion case.

- Raw uranium transport costs are set at roughly container-freight rates.

- The cost of U3O8 conversion to UF6 (uranium hexafluoride, which is processed by enrichment plants) is $14/kg U[51].

- The cost of UOx fuel fabrication is $270/kg heavy metal (HM, meaning uranium and plutonium)[52].

- The cost of MOx fuel blending and fabrication is $1800/kg heavy metal[53].

- The fraction of plutonium (Pu) in (fresh) MOx fuel is 7%[54].

- Spent fuel transport costs by ship are about $40/tHM-km[55].

- The cost of reprocessing is $1200/kg HM[56] except in Japan, where it is $3400/kg HM based on the costs of the existing Rokkasho plant[57].

- The effective average lag between placement of nuclear fuel in-service (in reactors) and its removal from spent fuel pools at reactors is 8 years.

- The cost of treatment and disposal of high-level wastes is $150/kg HM reprocessed, the mass of Pu separated during reprocessing is 11 kg/t HM in the original spent fuel, and the cost of storage and safeguarding of separated plutonium is $3000/kg Pu-yr[58].

- The average capital cost of dry casks (for UOx or MOx spent fuel) is $0.8 million/cask and the operating cost of dry cask storage is $10,000 per /cask-yr[59].

- The cost of interim spent fuel storage (total) is $360/kg HM placed in storage, and the cost of permanent storage of spent fuel is assumed to be $1000/kg HM placed in storage[60]. Permanent storage, however, is not implemented, and its costs are not charged, in any of the scenarios above by 2050.

2.3 Regional Nuclear Fuel Cycle Cooperation Scenario Results

2.3.1 Uranium Production and Enrichment

Over the period from 2000 through 2050, the countries of East Asia and the Pacific included in this study are projected to use a cumulative 1.5 to somewhat under 1.7 million tonnes of natural uranium in the BAU capacity expansion case, with usage under Scenario 4 about 7 percent higher than in Scenarios 1 and 2. Producing these quantities of uranium will require the extraction of about 30 (Scenarios 2 through 4) to 280 million tonnes (Scenario 1) of uranium ore, with extraction in Scenario 1 being much higher because more of the ore is mined domestically, rather than being sourced from higher-grade Canadian (and other) deposits. As large as these figures seem, they are dwarfed by the annual volume of coal extracted in China alone in a single year (over 3.5 billion tonnes in 2011[61], though of course Chinese coal-fired power plants generated substantially more power during 2011 than did all of the reactors in the region combined). Milling the uranium needed for reactors in the region will require about 1.6 billion cubic meters of water over the period from 2000 through 2050, which, to put the level of resource use in perspective, is about half of one day’s discharge of water from the Yangtze River to the ocean, or about a tenth of annual domestic water use in Japan.

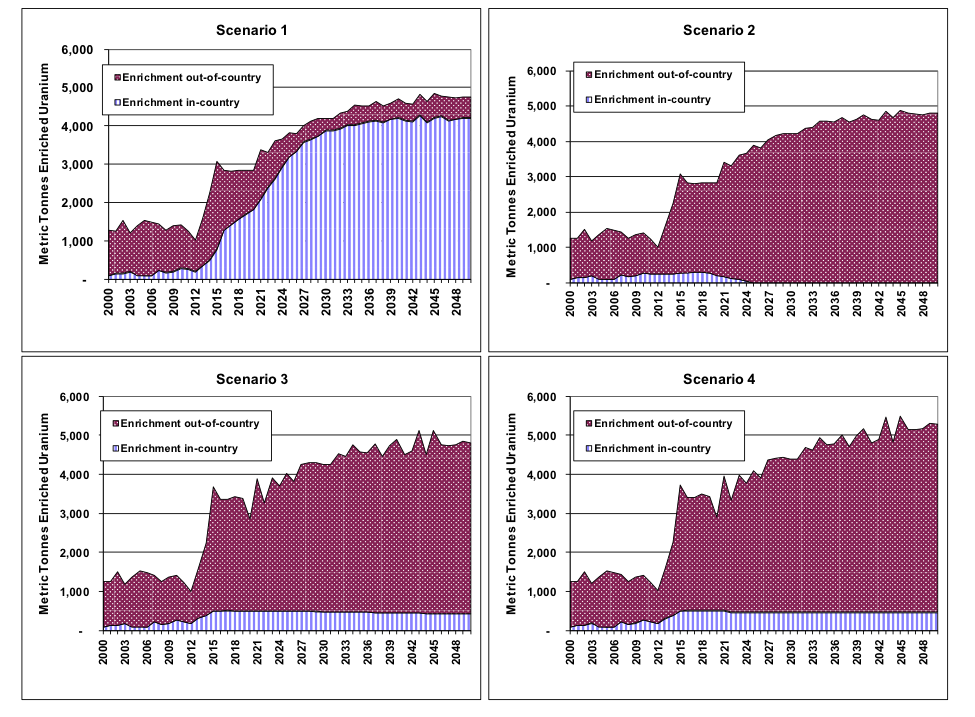

The enrichment services requirements for the BAU paths across scenarios are about 33 million kg SWU in 2050 in Scenarios 1-3, and about 37 M for Scenario 4 (which includes no MOx use). For the MAX generation capacity expansion path, needs rise to about 60 M SWU/yr in 2050 in scenarios without substantial MOx use, and are about 16 percent less in scenarios with MOx use. For the MIN path, requirements fall slowly from a maximum of about 20 million SWU in the 2020s to about 17 million SWU in 2050.

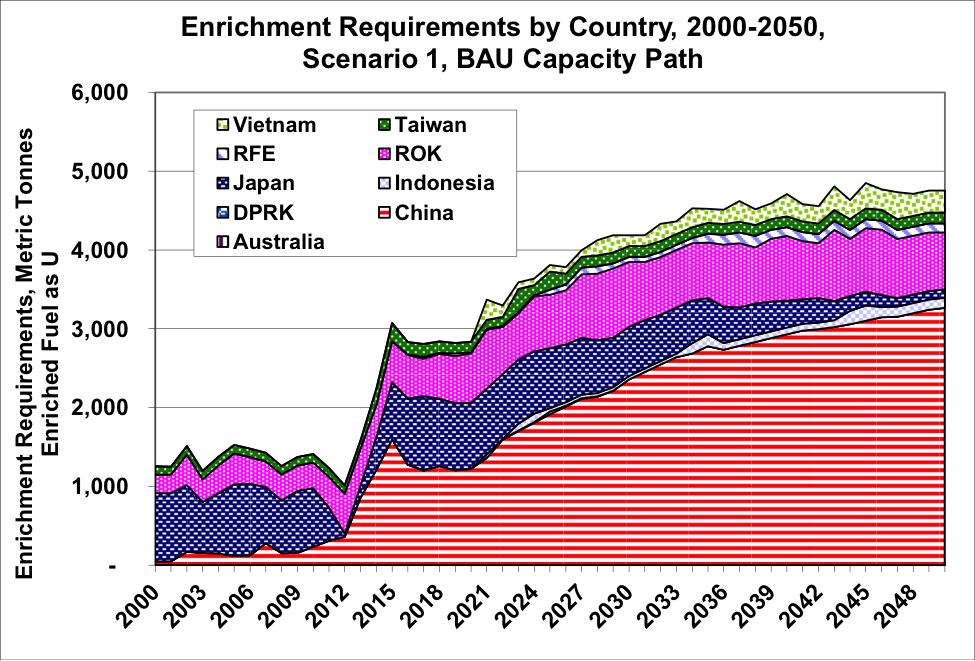

Under Scenario 1, additional enrichment capacity in the countries of the region will be required under all nuclear capacity expansion paths. Under other scenarios, global enrichment capacity by 2015 would need to be expanded to meet 2050 regional plus out-of-region enrichment demand under the BAU or MAX expansion paths. Under MAX expansion path and Scenario 1, China alone would need to build new enrichment capacity by 2050 approximately equal to half of today’s global capacity. Under the MIN expansion path, however, international enrichment facilities extant as of 2015 are likely sufficient to meet regional and out-of-region demand without significant expansion. Figure 3 summarizes the required regional volume of enrichment service required, both in-country and out-of country (that is, from regional or international facilities), for the period from 2000 through 2050 for each of the four scenarios. Figure 4 shows enrichment requirements over time by country. Though the ROK and Japan account for almost all enriched uranium needs now, China’s demand for enrichment will outstrip the rest of the region’s by 2030.

Figure 3: Requirements for Enriched Uranium by Scenario, Adjusted for MOx Use, BAU Nuclear Capacity Expansion Path

Figure 4: Requirements for Enriched Uranium by Country, Scenario 1, Adjusted for MOx Use, for the BAU Nuclear Capacity Expansion Path

2.3.2 Spent Fuel Production

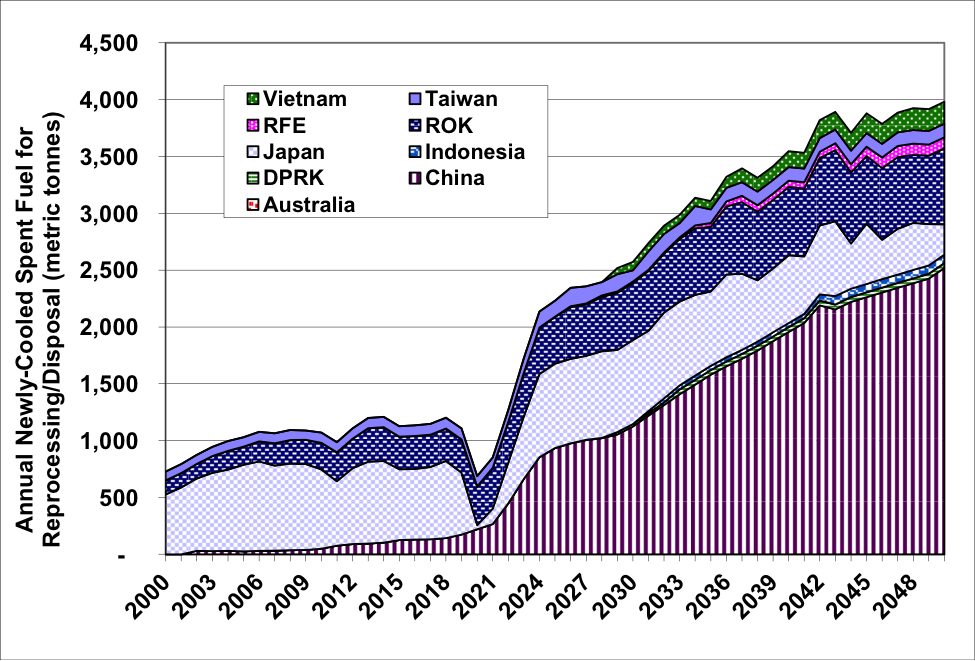

Figure 5 summarizes cooled spent fuel (UOx fuel only) production by country in Scenario 1 for the BAU capacity expansion path. By 2050, an annual volume of about 4000 tonnes of spent fuel regionwide will be cooled and ready for storage, reprocessing, or disposal. An additional 300 tonnes per year of MOx spent fuel will be cooled and require further management—but likely somewhat different management than UOx fuel, due to its different radiological properties) in 2050, with all cooled MOx fuel coming from Japan, China, and the ROK. Note, in Figure 5, the dip in cooled spent fuel production corresponding to the very low capacity factors for nuclear power in Japan in the aftermath of the Fukushima accident.

Figure 5: Production of Cooled Spent UOx Fuel by Year and by Country, Scenario 1 and BAU Nuclear Capacity Expansion Path

2.3.3 Spent Fuel Management

The increase in production of spent fuel has implications for the sufficiency of space for storage of spent fuel at reactors (spent fuel pools) and other facilities. In Scenario 1 under the BAU nuclear capacity expansion path, China, Japan, and the ROK will require new spent fuel storage capacity by the early 2020s or sooner (Japan and the ROK), and the mid-2030s (China). By 2050, storage, disposal, or reprocessing for over 3500 THM of spent fuel will need to be added annually, with about two thirds of that requirement in China. In the absence of regional cooperation on spent fuel management, the countries of East Asia, and in particular Japan, the ROK, and China, will in the next 10 to 20 years need to begin opening a large amount of out-of-reactor-pool spent fuel storage or disposal space, or develop the same equivalent amount of storage space in reprocessing facilities. This result is based, as noted above, on the assumption that new reactors will (mostly) be designed with 15 years of spent fuel storage capacity. Though it may be that new nuclear plants will be designed with larger spent fuel pools, this tendency may be tempered by consideration of the risks of at-reactor pool storage of large quantities of spent fuel, particularly when, as in many existing plants in Northeast Asia, spent fuel pools are “dense packed” with fuel rod assemblies. These risks were underscored by the damage to spent fuel in pool storage that occurred during the Fukushima Plant I accident in Japan starting in March 2011. Given the recent history of public opposition to new nuclear sites in Japan and the ROK, one would expect the process of developing new storage/disposal/reprocessing facilities to be difficult. China, with more lightly-populated area than the ROK or Japan, and less of a tradition of civic involvement, may find an easier path to siting such facilities. On the other hand, in the twenty years between now and when China will need such facilities, and given the recent trend of a growing civil society voice in key issues, spent fuel management facilities may also become progressively harder to site in China as well.

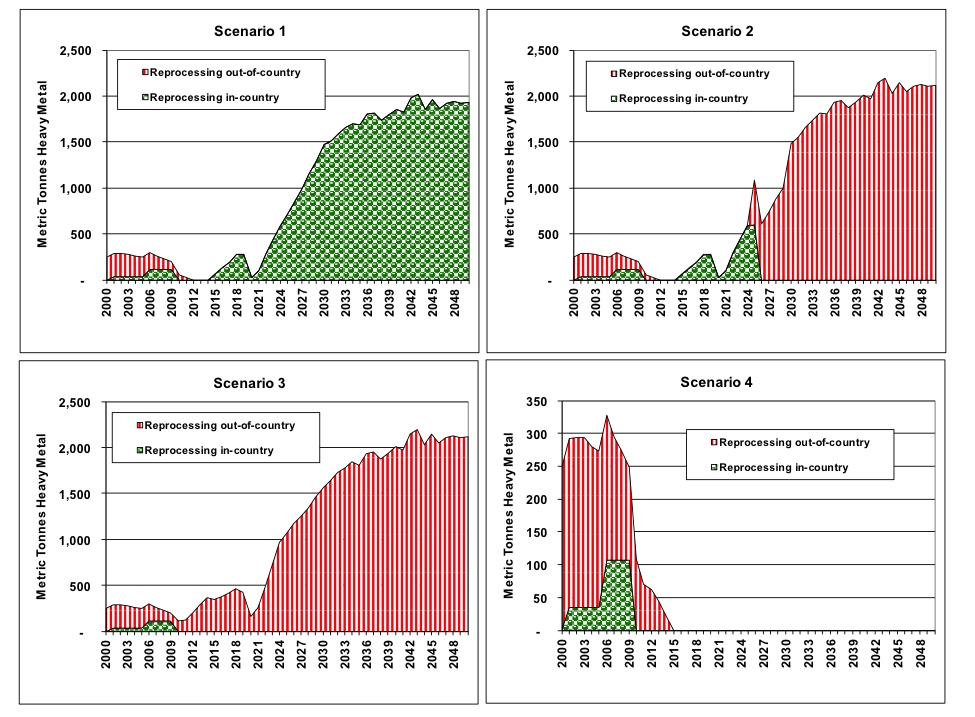

Figure 6 summarizes the region-wide use of reprocessing over time in each of the four Scenarios. A similar amount of reprocessing takes place in each of Scenarios 1 through 3, rising to about 2000 tonnes of heavy metal annually by 2050, but reprocessing in Scenario 1 takes place mostly in the countries of the region, while in Scenarios 2 and 3 reprocessing is mostly done either outside the region, or in shared reprocessing facilities in the region. In Scenario 4, as a result of the scenario assumptions, no reprocessing takes place after about 2016. Note that the scale in the graph for Scenario 4 is one-tenth the scale in the other three panels of Figure 8. A combination of active reprocessing and low growth in nuclear generation capacity yields large inventories of plutonium—on the order of 200 tonnes. Scenario 1 coupled with the “MAX” capacity expansion path produces a maximum regional inventory of plutonium of about 100 tonnes by 2038, but most of that inventory is used in MOx fuel by 2050, with little remaining by that time. Plutonium inventories remain at about 73 tonnes in all Scenario 4 capacity variants from about 2015 on. Placed in perspective, any of these quantities of Pu are sufficient that diversion of even a few hundredths of one percent of the total regional stocks would be enough to produce one or more nuclear weapons.

Figure 6: Region-wide Quantities of Spent Fuel Reprocessed by Year by Scenario, BAU Nuclear Capacity Expansion Path

2.4 Relative Costs of Scenarios

Along with the inputs to and outputs of nuclear fuel cycle facilities, the estimated costs of key elements of the nuclear fuel cycle have been evaluated for each combination of scenario and nuclear capacity expansion path. In general, though not in every case, “levelized” costs have been used, expressed, for example, on a per-tonne-heavy metal processed basis, to include a multitude of operating and maintenance as well as capital costs, often for very long-lived facilities. In other cases market trends in prices have been extrapolated, for example, for uranium prices and enrichment services, while providing for the option of modeling different price trends. All costs in the figures in this section are provided in 2009 dollars. The figures below focus on the results of the BAU nuclear capacity expansion path. As with other parameters, cost estimates are in many cases by their very nature quite speculative, as they often specify costs for technologies that have not yet been commercialized (permanent waste storage, for example), or are commercialized but practiced in only a few places in the world (reprocessing and high-level waste vitrification, for example), or are subject to regulatory oversight with the potential to considerably change costs, or for which specific costs were not immediately available for this analysis (such as most nuclear materials transport costs). As such, the costs estimates provided here should be taken as indicative only, for use primarily in comparing regional scenarios.

Not yet included in the cost analysis summarized here are the costs of nuclear generation, apart from fuel-related costs. These costs have been omitted (capital costs and O&M costs, for example) in analyses thus far because a full comparison of different nuclear paths also requires inclusion of the capital costs of other electricity generation sources and of other methods of providing energy services (such as energy efficiency improvements) that might be included in a given energy sector development path for a given country. It should be noted, however, that using MOx fuel in some of the region’s reactors will require modifications in reactor design and operation that will vary in cost by plant, but will likely be in the range of tens of millions of dollars in capital costs and tens of millions of dollars in annual operations costs, per reactor (see, for example, Williams, 1999). These costs would accrue to scenarios with substantial MOx use, but not to scenarios where reprocessing (and MOx use) is avoided.

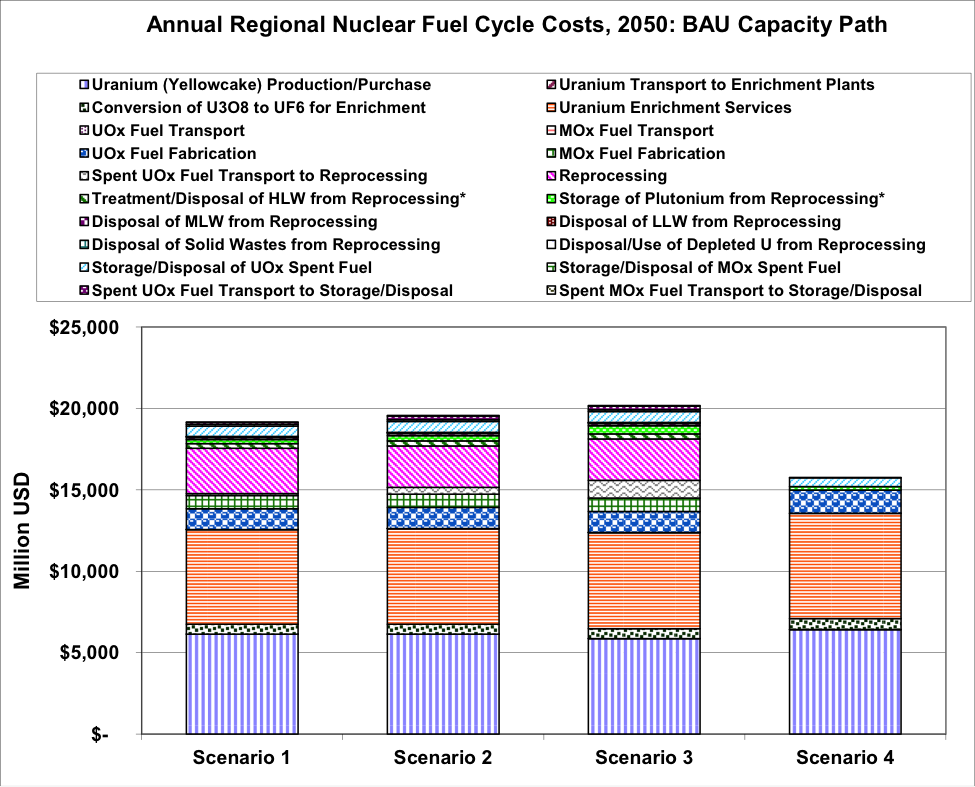

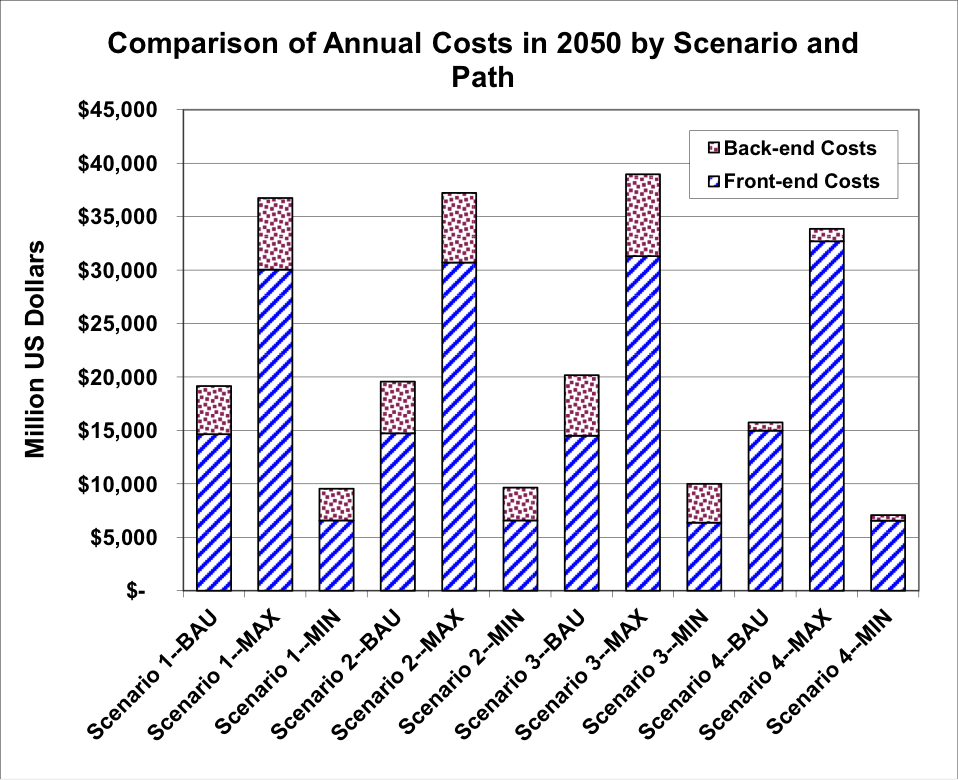

Initial highlights of the cost results summarized as annual costs in 2050 (Figure 10) include:

- Uranium mining and milling costs for the region are estimated at $5.9 to $6.4 billion per year by 2050, with the inclusion of reprocessing in Scenarios 1 through 3 reducing costs only modestly (a few percent) relative to Scenario 4.

- Natural uranium transport costs, at an estimated 1 to 6 million dollars per year in 2050, are a negligible fraction of overall costs.

- Uranium conversion costs range from 610 to 670 million dollars per year by 2050 for the countries of the region.

- Uranium enrichment costs for the region are on the same order of magnitude as mining and milling costs, at an estimated at $5.9 to $6.5 billion per year by 2050, with the inclusion of reprocessing in scenarios again reducing costs only modestly.

- UOx fuel fabrication costs are estimated at $1.3 to $1.4 billion annually by 2050.

- Though the quantity of MOx fuel used is much lower than that of UOx fuel, MOx fabrication costs are estimated at about $810 million annually by 2050 in Scenarios 1 through 3 where MOx is used.

- Reprocessing costs range from $2.5 to 2.8 billion per year in those Scenarios (1 through 3) that feature reprocessing.

- Treatment of high-level wastes from reprocessing adds $290 to 320 million per year to the costs of Scenarios 1 through 3, with treatment of medium-level, low-level, and solid wastes from reprocessing, and of uranium separated from spent fuel during reprocessing (less uranium used for MOx fuel) adding an aggregate $170 to 190 million per year to costs by 2050.

- Plutonium storage costs range from about $220 to $500 million/yr in 2050, with those scenarios that result in higher Pu inventories showing higher costs.

- Interim storage of non-reprocessed spent fuels (and of MOx fuel), in Scenarios 1 through 3, has estimated costs in 2050 of $750 to $780 million per year. In Scenario 4, using Dry Cask Storage, estimated costs in 2050 are about $540 million per year, or somewhat lower, though the amount of spent fuel being handled in Scenario 4 does not include the fuel sent to reprocessing. Estimated costs for transportation of spent fuel in are about $140 million annually in 2050 in Scenario 1, and about $260 million/yr in Scenarios 2 and 3, and $18 million/yr in Scenario 4.

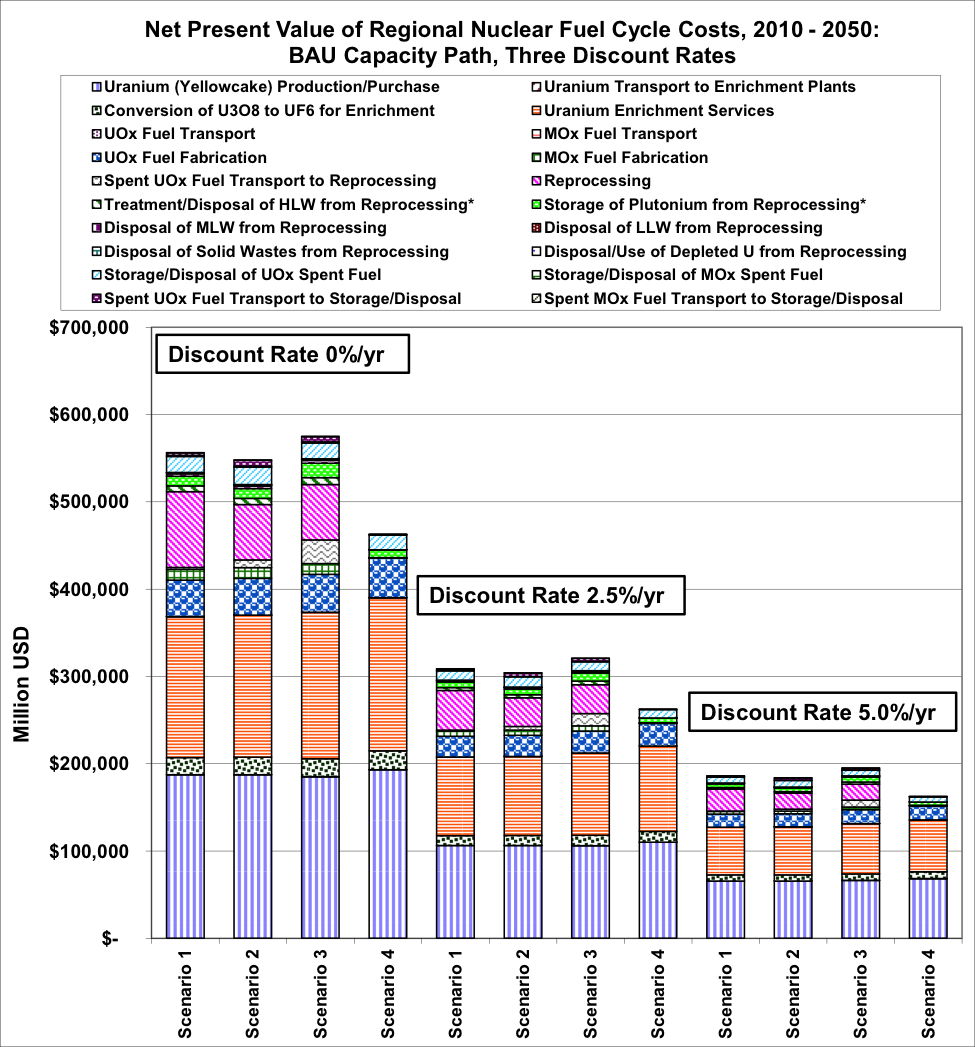

Overall, the conclusion from the above—similar to the conclusion that a number of other researchers have reached using per-unit costs (not from regional scenarios), is that reprocessing of spent fuel results in much higher costs—higher by on the order of $4 billion per year or more (about 20 percent), region-wide, in 2050—than using dry-cask storage and avoiding reprocessing of spent fuel, as shown in Figure 7. Figure 8 shows net present value costs from 2010 through 2050 (calculated with three different discount rates) for the nuclear fuel cycle elements. Scenario 1 through 3 yields total costs that about 14 to 19 (at a discount rate of 5.0 percent/yr) to 19 to 23 percent (at a zero discount rate) higher overall than in the least expensive scenario (Scenario 4). The absolute cost difference between scenarios declines somewhat as the discount rate used increases. Results at three different real discount rates are shown to reflect a range of potential perspectives as to the time value of money in nuclear investments. Present interest rates in Japan, for example, are near zero. In addition, one could argue that as investments with decidedly intergenerational implications, nuclear fuel cycle costs should be evaluated with a near-zero, zero, or even negative discount rate (see, for example, Hellweg et al, 2003).

Figure 7:

Figure 8:

2.5 Energy Security Attributes Comparison of Scenarios

The broader energy security definition referred to earlier in this Working Paper was used to develop a multiple-attribute method of compare national energy policy scenarios. This method was adapted to compare the energy security attributes of the four regional nuclear fuel cycle scenarios developed and evaluated as described above. It should be emphasized that while many different attributes and measures could be chosen for this analysis, the approach taken here has generally been to focus on attributes that are significantly different between scenarios, in order to provide guidance on the key policy trade-offs involved in choosing one scenario over another. Key results of this comparison are as follows:

Energy supply security: Arguably, Scenario 1, in which the major current nuclear energy nations of the region own and run their own enrichment and reprocessing facilities, provides greater energy supply security on a purely national level. On a regional level, depending on the strength of the agreements developed to structure regional cooperation on nuclear fuel cycle issues, Scenarios 2 and 3, and possibly 4, may offer better energy supply security. Scenarios 3 and 4 also offer the added security of shared fuel stockpiles.

Economic security: Scenarios including reprocessing have significantly higher annual costs, when viewed over the entire fuel cycle, than the scenario without reprocessing. The additional cost is still, however, only a relatively small fraction of the cost of nuclear power as a whole. The use of reprocessing and related required waste-management technologies may, however, expose the countries of the region to additional economic risks if the technologies have costs that are unexpectedly high (as has been the case, for example, with Japan’s Rokkasho reprocessing plant). In addition, the required additional investment, probably by governments or backed by governments (tens of billions of dollars, at least) in facilities related to fuel reprocessing may divert investment from other activities, within the energy sector and without, of potentially more benefit to the long-term health of the economies of the region. On the other hand, development of in-country and in-region nuclear facilities will have its own job-creation benefits in the nuclear industry and some related industries.

Technological security: Scenario 4, which depends on proven dry-cask storage, depends the least on the performance of complex technologies, but implicitly also depends on future generations to manage wastes generated today. Since all of the other scenarios, however, depend on interim storage of spent fuels, plutonium, and high-level wastes from reprocessing, and thus imply dependence on a future means of safe disposal, the scenarios are not so different in this long-term outlook.

Environmental security: Scenarios 1 through 3 evaluated offer a trade-off between somewhat (on the order of several to 10 percent) less uranium mining and processing, with its attendant impacts and waste streams, relative to scenario 4, balanced by the additional environmental burden of the need to dispose of a range of solid, liquid, and radioactive reprocessing wastes. Differences between the scenarios with regard to generation of greenhouse gases and more conventional air and water pollutants are likely to be relatively small, and are inconsequential when compared with overall emissions of such pollutants from the economies of the region.

Social-Cultural security: To the extent that some of the countries of the region have growing civil-society movements with concerns regarding nuclear power in general, reprocessing in particular, and local siting of nuclear fuel-cycle facilities, Scenario 4 arguably offers the highest level of social-cultural security. This advantage has likely been exacerbated by the social/political fallout from the Fukushima accident, although the different countries of the region are finding and will find that the Fukushima accident has impacts of different types and magnitudes on social and cultural issues related to Fukushima. In some cases current laws—in Japan, for example—would have to be changed to allow the long-term at-reactor storage included in Scenario 4, and changing those laws has its own risks.

Military security: From a national perspective, safeguarding in-country enrichment and reprocessing facilities in Scenario 1, including stocks of enriched uranium and (especially) plutonium, puts the largest strain on military (or police) resources. Those responsibilities are shifted largely to the regional level in Scenario 2, and to the international level in Scenario 3, with less stress on national resources, but more on the strength of regional and international agreements. The level of military security (guards and safeguard protocols) required of Scenario 4 is arguably considerably less than in the other scenarios.

3 Summary of Regional Nuclear Fuel Cycle Cooperation Scenario Results

The results of the regional scenario evaluation above indicate that Scenario 4, which focuses on at-reactor dry cask storage and coordinated fuel stockpiling, but largely avoids reprocessing and mixed-oxide fuel (MOx, that is, reactor fuel that uses a mixture of plutonium reprocessed from spent fuel and uranium and as its fissile material) use, results in lower fuel-cycle costs, and offers benefits in terms of social-cultural and military security. These results are consistent with (and, indeed, draw ideas and parameters from) broader studies by other research groups, including, for example, the joint work by the Harvard University Project on Managing the Atom and the University of Tokyo Project on Sociotechnics of Nuclear Energy.

That said, there are definite trade-offs between scenarios. Scenario 1, by using much more domestic enrichment and reprocessing than the other scenarios, arguably improves energy supply security for individual nations, but results in higher technological risk due to national reliance on one or a small number of enrichment and reprocessing plants, rather than the larger number of plants that constitute the international market. Scenario 1 would also raise significant proliferation concerns (not the least of which would be the DPRK’s reaction to ROK enrichment and reprocessing). Scenario 1 also results in the build-up of stockpiles of plutonium (Pu) in each of the nations pursuing reprocessing. Though the magnitude of the plutonium stockpiles, and the rate at which they are used, varies considerably by nuclear path and scenario, the quantities accrued, ranging from about 90 to about 200 tonnes of Pu at a maximum in Scenarios 1 through 3 in the years around 2040, are sufficient for tens of thousands of nuclear weapons, meaning that the misplacement or diversion of a very small portion of the stockpile becomes a serious proliferation issue, and thus requires significant security measures in each country where plutonium is produced or stored. Scenario 4, without additional reprocessing, maintains a stockpile of about 70 tonnes of Pu from about 2010 on. This still represents a serious proliferation risk, but does not add to existing stockpiles or create stockpile in new places.

Scenarios 1 through 3, which include reprocessing, result, as noted above, in higher annual costs-about $4 billion per year higher in 2050 relative to Scenario 4, over the entire region. Scenarios 1 through 3 reduce the amount of spent fuel to be managed substantially—by 50 percent or more over the period from 2000 through 2050, relative to Scenario 4—but imply additional production of 5600 to 6400 cubic meters of high-level waste that must be managed instead (versus about 360 cubic meters in Scenario 4). This in addition to medium- and low-level wastes from reprocessing, and wastes from MOx fuel fabrication that must be managed in significant quantities in Scenarios 1 through 3, but not in Scenario 4. Scenarios 1 through 3 offer a modest reduction—less than10 percent in for the BAU nuclear capacity paths case—in the amount of natural uranium required region-wide, and in attendant needs for enriched uranium and enrichment services. This reduction is not very significant from a cost perspective unless uranium costs rise much, much higher in the next four decades. The quantities of electricity and fuel used for uranium mining and milling, as well as production of depleted uranium, are generally somewhat lower under Scenarios 1 through 3 than under Scenario 4, though results for Scenario 1 differ from Scenarios 2 and 3 because of the emphasis on sourcing uranium from domestic mines in the region. Figure 9 shows aggregated front-end (fuel preparation) and back-end (spent fuel management) costs by Scenario and for each of the three nuclear capacity paths for the region.

Figure 9: Summary of Year 2050 Annual Costs by Scenario and by Nuclear Capacity Expansion Path

Scenarios 2 and 3, though they include reprocessing, place more of the sensitive materials and technologies in the nuclear fuel cycle in regional and international facilities, and as a consequence, are likely to be superior to Scenario 1 in terms of reducing proliferation opportunities, reducing security costs, and increasing the transparency of (and thus international trust in) fuel cycle activities. The costs of Scenarios 2 and 3 shown in this analysis are not significantly different, overall, from those of Scenario 1, but a more detailed evaluation of the relative costs of nuclear facilities (particularly, enrichment and reprocessing facilities) in different countries, when available, might result in some differentiation in the costs of these three scenarios. Overall, however, although the total costs of the scenarios may vary by several billion dollars per year, it must be remembered that these costs are inconsequential to the overall annual costs of electricity generation in general. In round terms, if one assumes that the total electricity demand in East Asia in 2050 is on the order of 20,000 TWh, or about three times electricity demand in the countries in the region as of 2011, and that the per-unit total cost of electrical energy at that time is on the order of 10 US cents/kWh (perhaps somewhat greater than the average in the region today, but possibly an underestimate for 2050), then the implied total cost of electricity supplies in 2050 in the countries under consideration in this Working Paper is on the order of $2 trillion per year. The nuclear-related costs considered here are therefore just a percent or so of the total, and the differences between scenarios is a just fraction of a percent. Both of these values are easily lost in the margin of uncertainty regarding future power costs.

Scenarios 2 and 3 result in significantly more transport of nuclear materials—particularly spent fuel, enriched fuel, MOx fuel, and possibly high-level wastes around the globe, likely by ship, than Scenario 1, though there would be somewhat more transport of those materials inside the nations of East Asia in Scenario 1.

The scenarios described and evaluated above have, of necessity, to a certain extent suspended consideration of national and international political and legal constraints in order to focus on alternatives for regional fuel cycle management. It is more than clear, however, that there are substantial legal and political constraints to regional cooperation on nuclear fuel cycles, and that these constraints will either limit the opportunities for cooperation, or need to be overcome in some way, in order to allow regional arrangements to proceed. These constraints include (but are unlikely to be limited to) legal and/or political constraints on regional spent fuel management, enrichment, and integrated facilities. Specific discussion of these issues is beyond the scope of this article, but will play a crucial role in determining the practicality of specific cooperation schemes.

4 Conclusions

Nuclear power will certainly continue to play a significant role in the economies of the countries of the East Asia and Pacific region for decades to come, but the extent of that role, and how the various cost, safety, environmental, and proliferation-risk issues surrounding nuclear power are and will be addressed on the national and regional levels, is not at all certain, and, in the wake of both the Fukushima accident and a host of recent leadership changes, is perhaps more uncertain than it has been in decades. The analysis summarized above indicates that different policy choices today, particularly with regard to cooperation between nations on nuclear fuel cycle issues, can lead to very different outcomes regarding the shape of the nuclear energy sector—and of related international security arrangements—over time. Regional cooperation on nuclear fuel cycle issues can help to enhance energy security for the participating countries, relative to a scenario in which several nations pursue nuclear fuel cycle development on their own. From a number of energy security perspectives, however, a regional nuclear fuel cycle approach (such as that modeled in Scenario 4) that rapidly phases out reprocessing and MOx fuel use, and uses interim spent fuel storage in dry casks (or similar technologies) to manage spent fuel until indefinite storage facilities–potentially including “deep borehole disposal”[62]–has significant advantages. An approach that avoids reprocessing and MOx fuel use would be less expensive as well, though placed in perspective, the $4 billion or so saved annually in 2050 under Scenario 4 relative to other scenarios is just a small fraction of the overall cost of nuclear power, and a tiny fraction of the overall costs of power in general. What this means that relative fuel cycle costs, at least for the range of LWR-based fuel cycles cooperation/non-cooperation options explored here, should in most cases play a trivial role in decisions about nuclear spent fuel management, and the other considerations described here should thus dominate the policy development process. Of these, it is likely to be the least quantifiable considerations—social and cultural factors, preventing nuclear weapons proliferation, nuclear safety, and military security issues—that are likely to be the most important to decisions regarding nuclear spent fuel policy. Unfortunately, these are the very issues that are some of the most difficult to address, particularly in the many instances where addressing those issues require a coordinated international, and intercultural, response.