by Kae Takase

29 April 2014

From the Governance Design Laboratory (GDL), originally published on December, 2013.

I. INTRODUCTION: Brief history of the japanese energy sector

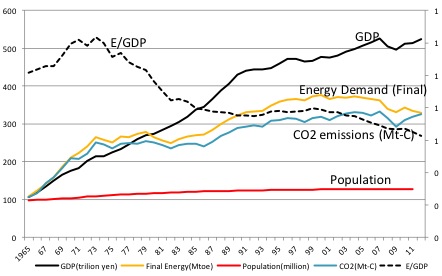

The Japanese economy, as measured by gross domestic product (GDP) grew rapidly during the 1960s through the1980s. In 1991, what has been called Japan’s “ bubble economy”, crashed, ushering in an era of much slower economic growth that continues to this day. Figure 1 shows trends in key energy and economic indicators for Japan. Energy consumption per unit of GDP decreased after the first global “oil crisis” (a period during which international oil prices increased rapidly due to restricted supplies and price controls by major producers) in 1973. After the first oil crisis, Energy demand in Japan continued to increase in most years, but at a lower rate than GDP. National carbon dioxide (CO2) emissions also continued to increase, but not as by much as energy demand, due in part to nuclear power development from the 1970s onward.

Source: 1965-2011, EDMC/IEEJ, EDMC Handbook of Energy & Economic Statistics in Japan 2013 (*Data for 2012 estimated by GDL from various sources.)

Figure 1: Trends in Population, GDP, Energy Demand, and CO2 Emissions in Japan (1965-2912)

Figure 1: Trends in Population, GDP, Energy Demand, and CO2 Emissions in Japan (1965-2912)

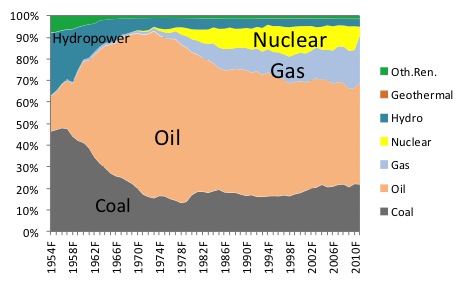

Japan’s primary energy supply has shifted from an alliance on coal and hydropower in 1950s to oil and coal by 1970. After the 1st and 2nd oil crises in 1973 and 1981, the use of nuclear power and natural gas, mostly imported as liquefied natural gas and used directly as an end use fuel and for power generation, increased to provide 20-30% of primary energy supply, as shown in Figure 2. Source: EDMC/IEEJ, EDMC Handbook of Energy & Economic Statistics in Japan 2013

Figure 2: Primary energy supply by sources (% of kcal)

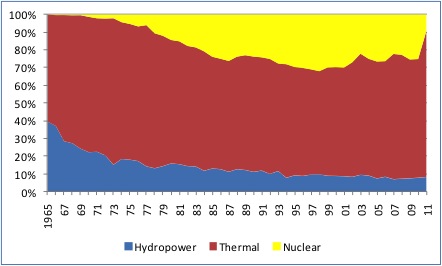

Electricity was generated primarily in thermal and hydroelectric power plants until commercial nuclear power plants in Japan started operating in 1970. Nuclear power accounted for almost 30 percent of total generation until the Fukushima Daiichi accident in March of 2011. In the wake of the Fukushima accident, all of the remaining nuclear power plants in Japan were shut down for extensive safety assessments and retrofitting, as reflected in the much-reduced nuclear fraction for 2011 that appears in Figure 3. As of this writing, none of Japan’s nuclear reactors are currently on line. Source: EDMC/IEEJ, EDMC Handbook of Energy & Economic Statistics in Japan 2013

Figure 3: Electricity Generation by Source (% of kWh generated)

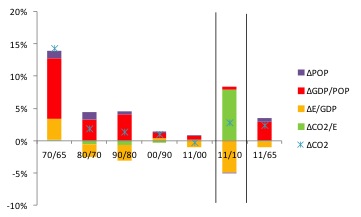

Japan’s CO2 emissions trends can be decomposed into four contributing factors. The so-called “Kaya identity” expresses the annual change in energy use as the summation of the change in population growth, GDP per capita growth, energy use per unit of GDP, and CO2 emissions per unit of energy use.[1] Figure 4 shows the contributing factors to Japan’s trends in CO2 emissions from 1965 through 2011 in ten-year increments (except 2010 through 2011). In general, the energy intensity of GDP (E/GDP)— reflecting a combination of true energy efficiency increases and reduced energy intensity due to continued restructuring of Japan’s economy away from heavy industries, has declined overall since 1965, although it rose before the first oil crisis and rose slightly during the period from 1990 to 2000. As such, during the1965-2011 period as a whole, population growth and GDP per capita growth have been the factors driving overall energy consumption growth, but fall in energy use per GDP has worked to dampen overall growth in energy consumption. Since the year 2000, CO2 emissions have not increased (in fact, have slightly decreased) in Japan, largely because the typical driving factors (population and GDP per capita) have not increased much, and at the same time, energy consumption per unit of GDP has decreased. In 2011, however, compared to 2010, energy consumption per unit of GDP decreased substantially, but the difference between the two years was mostly due to the hot summer and cold winter in 2010, which raised energy use in that year, and the impacts of the earthquake and tsunami of March 2011, which reduced energy use in 2011 though there was large growth in CO2 emissions per unit of energy use (CO2 intensity of energy) due in large part to the post-Fukushima shut-down of Japan’s nuclear reactor fleet. Source: 1965-2011, EDMC/IEEJ, EDMC Handbook of Energy & Economic Statistics in Japan 2012 (*Data for 2012 is estimated by GDL with various sources.)

Figure 4: Decomposition of factors for CO2 emissions (Population, GDP per capita, Energy per Unit GDP, CO2 per Energy Demand) in Japan using Kaya identity(1965-2011)

Nuclear Power Updates

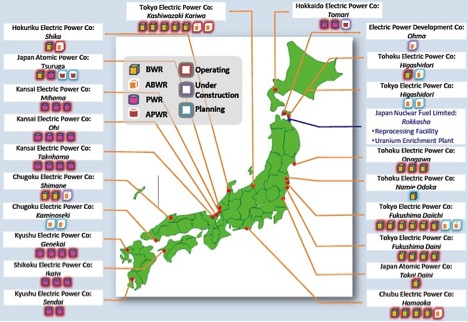

The first commercial nuclear power plants in Japan, Tsuruga unit #1 and Mihama unit #1, started operation in 1970, followed by the Fukushima Daiichi #1 plant in 1971. In all, during the 1970s, 20 nuclear power plants started operation in Japan. Figure 5 provides a map of the locations of the nuclear power plants and units in Japan. At present there are 50 nuclear reactor units at power plant sites in Japan, excluding Fukushima Daiichi units #1 to #4, which were damaged seriously following the March 11, 2011 Sendai earthquake.

Figure 5: Japan’s Nuclear Power Plant Fleet[2]

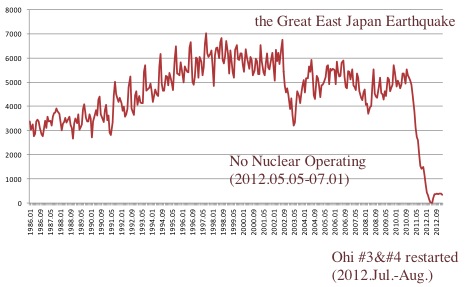

After the Fukushima accident, the number of nuclear power plants under operation decreased very rapidly. Many of the nuclear plants operating at the time of the accident automatically stopped operating at the time of the earthquake as safety systems were engaged, but after the accident, all of the remaining reactors were shut down for safety inspections. In practice, in Japan, nuclear power plants cannot be restarted, even if shut down for routine inspections, without the local government’s permission to restart the plant. This is not a legal regulation, but is conventional rule followed by nuclear plant owners and their local hosts. In the aftermath of Fukushima, local governments were reluctant to give permission to allow reactors to restart. As a result, by May, 2012, as shown in Figure 6, no nuclear power units were operating due to the difficulty of receiving permission to proceed with restart following inspections. In July and August, 2012, two units at the Ohi power station were restarted, but were shut down again when the time came for their next scheduled regular inspection, in September 2013. The newly established Nuclear Regulation Authority, Japan (NRA, Japan) released new regulatory guidelines for nuclear power plants in July, 2013, and as of late 2013 electric utilities were applying to restart reactors under those guidelines, and hoping for faster restarts. The approval process under the new guidelines, however, was likely to take one half to one year to complete, thus rapid restarts seemed unlikely. Operation of the Rokkasho reprocessing plant, which has been temporarily stopped due to various operational difficulties, is expected to eventually resume, in large part, because the governor of Aomori prefecture has protested and asked that all of the spent fuel now in storage at Rokkasho be moved out of Rokkasho if reprocessing should stop. Since Japan lacks the facilities to store the 3000 tonnes of spent fuel currently, complying with the request of governor’s request implies either restarting Rokkasho or embarking on an immediate program of building additional storage facilities, which is unlikely to be a rapid process, based on recent experience of difficulties in siting nuclear facilities in Japan.

Figure 6: Historical Trends of Nuclear Power Monthly Output in Japan, 1986 through late 2012 (1010 kcal)[3]

Update on Japanese Energy Policies

Following the elections of December 2012, the dominant political party changed from Democratic Party to the Liberal Democratic Party (LDP). As a result, that the Democratic Party energy policies, which included a plan, discussed and developed with the aid of a stakeholder group drawn from a number of different organizations, to phase out nuclear power in Japan by sometime in the 2020s, have essentially returned to the drawing board, and are being significantly revised. Meanwhile, however, the feed-in-tariff (FIT ) policy developed by the Democratic Party remained. Under the FIT, utilities are required to pay a premium to purchase power derived from most renewable electricity sources. Further, the tariff was set at high levels to provide incentives for various companies and groups to enter the renewable power business. Prime Minister Abe (LDP) has promised to deregulate electricity retail market fully by 2016. Currently, only large and middle-sized industrial and commercial consumers can only choose their electricity retailer. Deregulation is to be followed by vertical separation of utility functions during the period 2018-2020. The LDP and Prime Minister Abe’s policy is to restart nuclear power plants for which compliance with safety regulations has been confirmed. This is a significant departure from the policy developed by the Democratic Party when it was in power.

FIT (Feed-in Tariff)

The FIT program for rooftop photovoltaic panels (PVs) began in November, 2009, and was expanded to cover all renewable sources of electricity in July, 2012. Tariff levels for purchased power under the FIT have been set as described in Table 1.

Table 1: Japanese FIT Tariff Levels[4]

| Energy Source | Type | coverage of purchase |

Price (yen/kWh) |

||||

| 2012.7~2013.3 | 2013.4~2014.3 | 2014.4~2015.3 | Purchase Period (years) | ||||

| PV | less than 10 kW |

surplus |

42 yen/kWh |

38 |

37 |

10 |

|

|

(34 w/ Fuel Cells) |

(31 w/ Fuel Cells) |

(30 w/Fuel Cells) |

|||||

| 10 kW and larger |

all |

42+tax |

36+tax |

32+tax |

20 |

||

| Wind | Offshore |

all |

36+tax |

20 |

|||

| less than 20 kW |

all |

55+tax |

Same as previous year | Same as previous year |

20 |

||

| 20 kW and larger |

all |

22+tax |

20 |

||||

| Small Hydro | less than 200 kW |

all |

34+tax |

20 |

|||

| 200-1000 kW |

all |

29+tax |

20 |

||||

| 1000-3000 kW |

all |

24+tax |

20 |

||||

| Small Hydro utilizing existing water corridors | less than 200 kW |

all |

25+tax |

20 |

|||

| 200-1000 kW |

all |

21+tax |

20 |

||||

| 1000-3000 kW |

all |

14+tax |

20 |

||||

| Geothermal | less than 15,000 kW |

all |

40+tax |

Same as previous year |

15 |

||

| More than 15,000kW |

all |

26+tax |

15 |

||||

| Biomass | methane fermentation gasification |

all |

39+tax |

20 |

|||

| unused wood combustion 1) |

all |

32+tax |

20 |

||||

| wood combustion 2) |

all |

24+tax |

20 |

||||

| waste (non-wood) combustion 3) |

all |

17+tax |

20 |

||||

| recycled wood combustion 4) |

all |

13+tax |

20 |

||||

1) Using timber from forest thinning or regeneration cuts, approved as “unused”.

2) Using wood other than “unused” or “recycled”, such as waste wood from lumber milling or and imported waste wood, and agricultural residues such as palm chaff, and rice husks.

3) Burning biomass such as domestic wastes, sewage sludge, food waste, RDF (refuse-derived fuel), RPF (refuse paper and plastic fuel), and black liquor from wood pulp production.

4) Burning biomass such as construction and demolition waste.

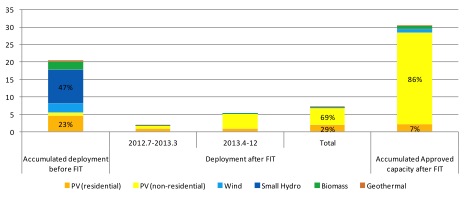

The tariff levels offered by the FIT are sufficient to be inviting to newcomers to the renewable power business. The total capacity of projects approved under the FIT reached 30 GW by the end of December, 2013, and operating capacity (newly introduced after the FIT) at that time reached 7.0 GW. 97% of the operating capacity is PV systems, thanks to their short lead times, but plans for development of other renewable sources of electricity are underway, as shown in Table 2 and Figure 7.

Table 2: Japanese FIT Approvals and Deployment by Technology through December, 2013 (GW)[5]

|

Accumulated deployment before FIT |

Deployment after FIT |

Accumulated Approved capacity after FIT |

|||

|

2012.7 -2013.3 |

2013.4-12 |

Total |

|||

| PV (residential) |

4.7 |

0.97 |

1.0 |

2.0 |

2.3 |

| PV (non-residential) |

0.90 |

0.70 |

4.1 |

4.8 |

26 |

| Wind |

2.6 |

0.063 |

0.011 |

0.07 |

1.0 |

| Small Hydro |

9.6 |

0.0020 |

0.0030 |

0.0050 |

0.24 |

| Biomass |

2.3 |

0.030 |

0.089 |

0.12 |

0.72 |

| Geothermal |

0.50 |

0.0010 |

0.00 |

0.0010 |

0.013 |

| Total |

21 |

1.8 |

5.3 |

7.0 |

30 |

1) Using timber from forest thinning or regeneration cuts, approved as “unused”.

2) Using wood other than “unused” or “recycled”, such as waste wood from lumber milling or and imported waste wood, and agricultural residues such as palm chaff, and rice husks.

3) Burning biomass such as domestic wastes, sewage sludge, food waste, RDF (refuse-derived fuel), RPF (refuse paper and plastic fuel), and black liquor from wood pulp production.

4) Burning biomass such as construction and demolition waste.

Figure 7: Japanese FIT Approvals and Deployment by Technology through December, 2013 (GW)

Deregulation of the Electricity Market

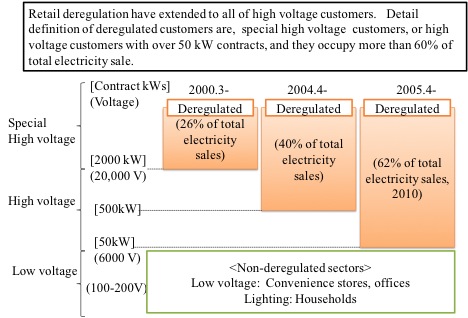

Japan’s retail electricity market is currently partially deregulated. Low voltage (less than 50 kW demand, served at 6000 Volts or less) customers have no choice but to purchase electricity from the utility designated to exclusively serve their area. Low voltage electricity sales were about 40% of total electricity sales in Japan as of 2010. Low voltage customers are small business such as convenience stores and offices, and households. The market for supplying electricity supply is partially open to non-regionally-dominant companies (that is, to electricity producers other than the major utility in the area). Since only 3-4 % of the retail market is occupied by non- regionally-dominant companies, the 10 regionally-dominant companies that have traditionally controlled electricity generation, transmission, and retail sales in Japan continue to substantially dominate Japan’s electricity markets, as shown in Figure 8.

Figure 8: Current situation of electricity deregulation in Japan[6]

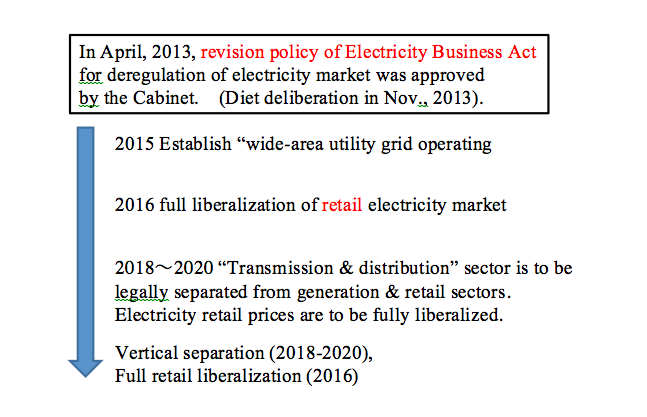

Continued deregulation, which has been promised by Prime Minister Abe, is planned to proceed in 3 steps, as shown schematically in Figure 9: Step 1: Revision of Electricity Business Act. This revision passed the Diet on Nov. 13, 2013, and enables inter-regional electric power interchange. It includes plans to establish a “wide-area utility grid operating organization” in 2015 to open up regional markets, and integrate electricity sales in Japan into one big market. Step 2: Retail Deregulation. Plans are to fully open retail electricity market by 2016. Low-voltage customers including households can choose retail companies or the supply plan that the retail companies provide. Plans are to submit a revision of the Electricity Business Act to enable this change to the Diet in 2014. Step 3: Vertical Separation. The “transmission and distribution” sector is to be separated from the electricity generation companies. The revision of the Electricity Business Act to accomplish vertical separation is to be submitted in 2015.

Figure 9: The Cabinet’s Plan for Electricity Sector Deregulation

Figure 9: The Cabinet’s Plan for Electricity Sector Deregulation

Despite opposition from electrical industry groups, Prime Minister Abe seems to have a strong will to proceed with the deregulation process.

Revision of LEAP Energy/Environment Model for Japan

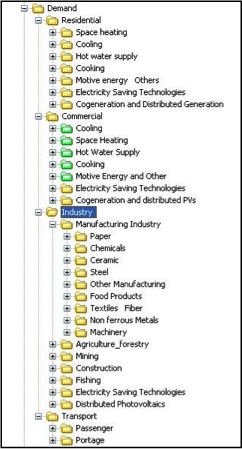

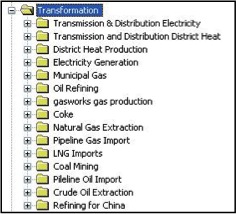

The LEAP (Long-range Energy Alternatives Planning system) model for Japan has updated been to a 2011 base year. Most LEAP data for recent years has been prepared using the “EDMC Handbook of Energy & Economic Statistics in Japan 2013” by EDMC/IEEJ. The LEAP Japan model has very a detailed demand and supply structure, reflecting the Japanese energy sector. The demand sector (see Figure 10) is divided into residential, commercial, industrial, and transport sectors, These are further divided as follows: ² The residential & commercial sectors are divided into 5 energy end-uses ² The industrial sector is divided into 13 subsectors. ² The transport sector is divided into passenger (passenger transport) and portage (freight transport). The energy supply (“transformation”) portion of the Japan LEAP model includes modules to simulate electricity generation, gas transformation, oil refining, electricity transmission, and other processes associated with production of end-use and intermediate fuels, as shown in Figure 11.

Figure 10: Demand structure of Japanese LEAP model

Figure 11: Supply structure of Japan LEAP model

LEAP Scenarios for Japan

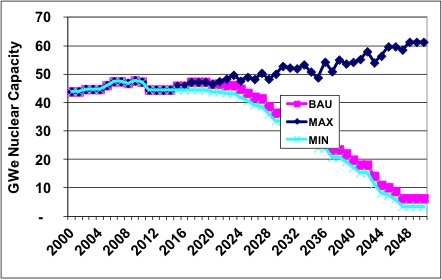

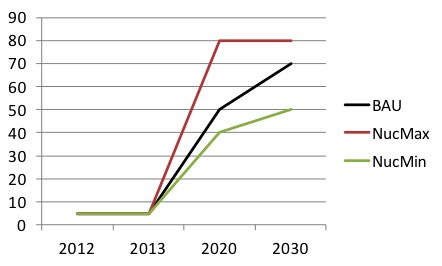

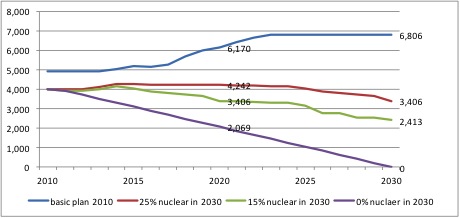

Within the Japan LEAP dataset, three scenarios for the future of nuclear power in Japan were prepared. A summary of the assumptions for this scenario is provided in Table 3. A common assumption in all three scenarios is that the Fukushima Daiichi nuclear units #1-4, which were severely damaged and contaminated with radioactivity in the accident following the Sendai earthquake and Tsunami, are to be decommissioned. In the BAU scenario, only two new nuclear plants are added to Japan’s fleet, both of which were under construction at the time of the Fukushima accident. In the BAU scenario, it is assumed that the Ohma is to start operations in 2015, with Higashidori starting in 2017. The addition of these plants might not, in fact, be realized due to strong opposition against nuclear power in Japan after the Fukushima accident. A reactor lifetime of 40 years or operation for existing and new nuclear units is assumed. Nuclear plants reaching the end of their operating lifetime are assumed not to be replaced with new nuclear plants. In the Maximum scenario, additional nuclear units are added as planned before Fukushima (addition of 17 plants), and the operational period is expanded to 50 years, which assumes that the utilities that run the plants are successful in receiving regulatory permission extend the operating lifetime of the reactors. In addition, as existing units reach the end of their operational lifetime, they are replaced with similar –sized (though updated) units. In the Minimum scenario, no additional plants are added from the present onward, and a 40-year operational lifetime is assumed for existing nuclear units. It is assumed, however, that nearly all of Japan’s existing reactors will be restarted soon. Figure 12 shows the resulting trends in nuclear capacity in Japan under the three scenarios.

Figure 12: Trends of Nuclear Capacity in 3 Scenarios

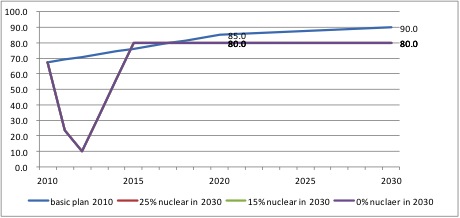

The assumed average capacity factors (maximum availability) for nuclear power plants in Japan under each of the three scenarios are shown Figure 13. By way of comparison, nuclear plant capacity factors in Japan typically ranged between 70 and 80 percent during the 1990s, but rarely exceeded 70 percent from 2002 until the Fukushima accident in 2011.

Figure 13: Average Capacity factor (maximum availability) of Nuclear Power Plants in Three Scenarios

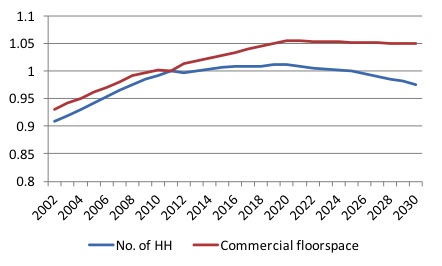

As shown in Figure 14, two of the main driving activities of energy demand in the residential and commercial sectors in Japan, namely, the number of households and total commercial floorspace, are assumed to decrease after 2020, as Japan’s population continues to decline from the peak levels reached in the last few years.[7]

Figure 14: Assumptions for Number of Households and Commercial Floorspace (same in all three scenarios)

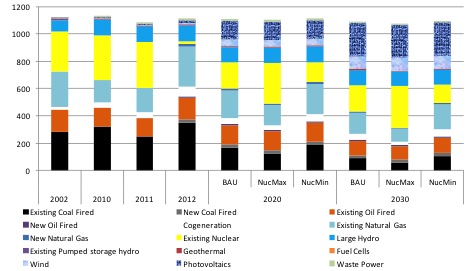

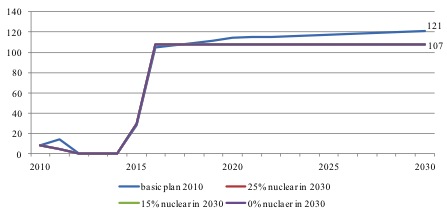

Final energy demand is common in all three scenarios considered, as only supply-side, nuclear capacity changes are implemented in Maximum and Minimum scenarios. As shown in Figure 14, total final energy demand is projected to decrease due to the decrease in the number of households and in commercial floorspace, as well as due to efficiency improvement in motor vehicles and elsewhere in the Japanese economy.  Figure 15: Final Energy Demand by Sector Figure 16 shows the historical division of electricity generation by source in several historical years and in each of the three scenarios in 2020 and 2030. Total generation is roughly the same in each case, but the nuclear fraction of generation is much higher in the NucMax (Maximum) case, while generation from coal, gas, and oil is much less than in the other two scenarios. In each case, electricity from PVs rises to a significant portion of the overall total.

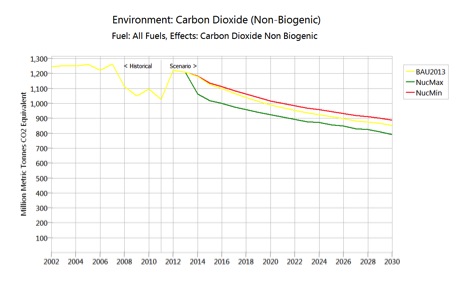

Figure 15: Final Energy Demand by Sector Figure 16 shows the historical division of electricity generation by source in several historical years and in each of the three scenarios in 2020 and 2030. Total generation is roughly the same in each case, but the nuclear fraction of generation is much higher in the NucMax (Maximum) case, while generation from coal, gas, and oil is much less than in the other two scenarios. In each case, electricity from PVs rises to a significant portion of the overall total.  Figure 16: Electricity Generation by Type of Power Plant, 3 Scenarios (TWh) Japan’s total CO2 emissions from the energy sector decrease in all three scenarios, but falls most rapidly in the Nuclear Maximum scenario, although the differences in emissions between the scenarios is relatively modest. The overall decline in emissions is due largely to non-fossil fuel energy deployment. The trends in emissions under the three scenarios are shown in Figure 17. If we compare the CO2 emissions of our scenarios with statistics published by Ministry of Environment (MOE), the BAU scenario shows a 7% reduction from 1990 levels, the Nuc Max scenario, shows a 12% reduction, and the Nuc Min scenario shows a reduction of 4%. (MOE statistics[8] show 1059 Mt of CO2 emissions from energy sources in 1990.)

Figure 16: Electricity Generation by Type of Power Plant, 3 Scenarios (TWh) Japan’s total CO2 emissions from the energy sector decrease in all three scenarios, but falls most rapidly in the Nuclear Maximum scenario, although the differences in emissions between the scenarios is relatively modest. The overall decline in emissions is due largely to non-fossil fuel energy deployment. The trends in emissions under the three scenarios are shown in Figure 17. If we compare the CO2 emissions of our scenarios with statistics published by Ministry of Environment (MOE), the BAU scenario shows a 7% reduction from 1990 levels, the Nuc Max scenario, shows a 12% reduction, and the Nuc Min scenario shows a reduction of 4%. (MOE statistics[8] show 1059 Mt of CO2 emissions from energy sources in 1990.)

Figure 17: CO2 Emissions in Japan, Three Scenarios

Nuclear Spent Fuel Scenarios

During the Nautilus Working Group Meeting in May, 2013, held in Beijing, the Japan Team assembled several spent fuel accumulation scenarios. These do not correspond exactly to the range of nuclear power scenarios described above, but represent a range of different possible outcomes for spent fuel accumulation in Japan. The Japan team consisted of Professor Tomochika Tokunaga of the University of Tokyo, Ms. Tomoko Murakami of the Institute of Energy Economics, Japan (IEEJ), and Kae Takase (the author of this paper).most of the information and basic data regarding nuclear power and spent fuel that was used in generating and evaluating these scenarios was provided by Ms. Tomoko Murakami (IEEJ), but the calculations of spent fuel arisings and accumulation described below were done by the author, and thus should not be interpreted as indicative of Ms. Murakami’s or IEEJ’s view of nuclear power and spent fuel futures in Japan.

Nuclear Power Scenarios for Spent Fuel Calculations

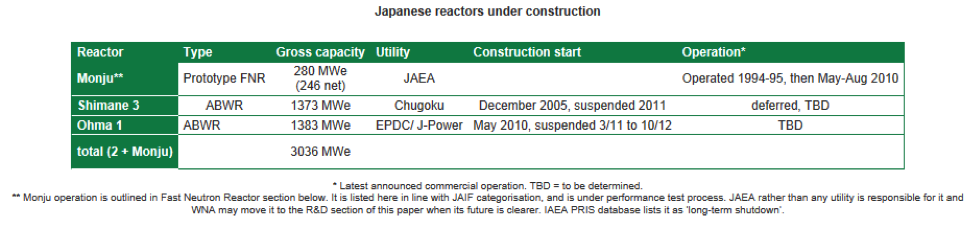

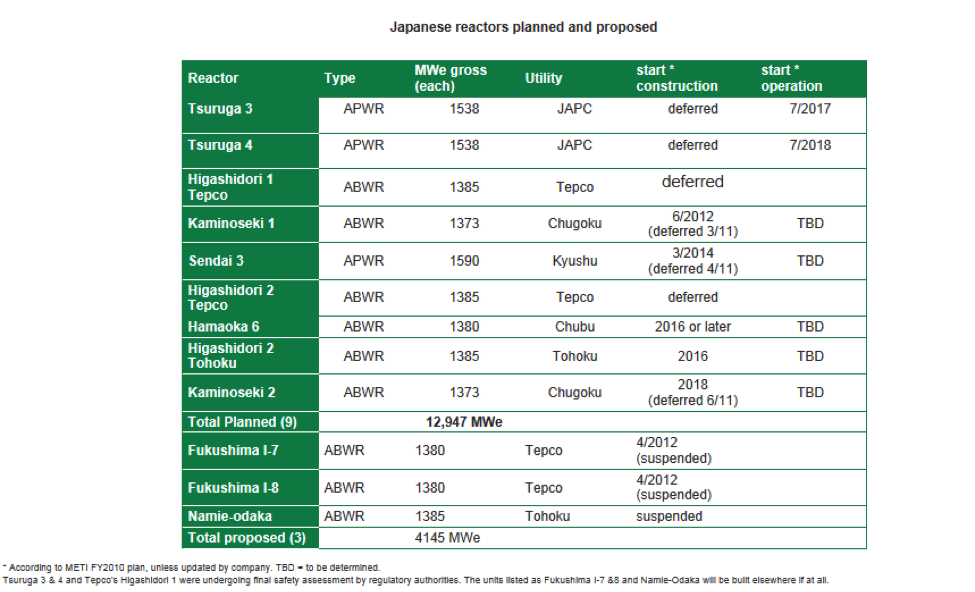

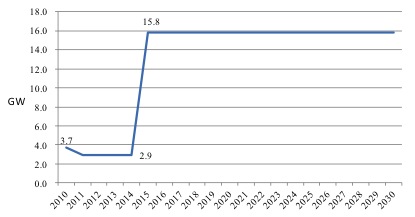

Four scenarios of future nuclear generation capacity were developed. Scenario 1 is an example case, prepared for comparison purposes, that projects what might have happened had there not been a Fukushima accident. In this case, 14 additional nuclear power plants[9] would have been added, it is assumed, and life extension is applied to all plants such that each operates for 60 years. In this case, the Fukushima plants all also continue to operate. In Scenario 2 to 4, all 10 units at the two Fukushima plants (6 plants in Fukushima Daiichi (#1), 4 plants in Fukushima Daini (#2)) are assumed to be shut down permanently following the accident in March, 2011. In Scenario 2 and 3, two units are added: those under construction at the Shimane plant (unit #3) and at Ohma. Shimane #3 is assumed to start operating in 2014, with Ohma starting in 2015. In Scenario 2, all plants are assumed to operate for 50 years. In Scenario 3, all plants will operate for 40 years. In Scenario 4, nuclear plants will be phased out such that no plants will remain in operation in 2030. Table 4 summarizes the assumptions in the four nuclear scenarios explored for the purpose of estimating spent fuel production, Table 5 lists the reactors under construction, planned, and proposed for Japan, and Figure 18 shows capacity trends for the four scenarios through 2030.

Table 4: Nuclear Spent Fuel Scenario Capacity Assumptions

| Scenario Description |

Fukushima Plants |

Additional Plants after 2011 |

Years of Operation |

| 1) Basic plan 2010 | Assumed no accident occurred | 14 plants |

60 years |

| 2) 25% nuclear in 2030 | Fukushima Daiichi (#1), Daini (#2) to be decommissioned after 2011 accident | 2 plants (Shimane unit #3 in 2014, Ohma in 2015) |

50 years |

| 3) 15% nuclear in 2030 | Same as above | Same as above |

40 years |

| 4) 0% nuclear in 2030 | Same as above | Same as above |

Plants shut down gradually so that no plants are operating in 2030 |

Table 5: Japanese Reactors under Construction, and Planned & Proposed[10]

Figure 18: Nuclear Power Capacity Scenarios for Estimation of Spent Fuel Production (10 MW) The assumed annual average capacity factors for the reactor fleets under the four different spent fuel scenarios are as shown in Figure 19, below. In Scenario 1, to approximate the previous energy basic plan (2010), the average capacity factor is assumed to increase to 90% in 2030. In the other scenarios, capacity factors decreases to 10% in 2012, consistent with actual experience post-Fukushima, then increase to reach 80% in 2015, maintaining that level until 2030. In reality, the actual capacity factor in 2013 was significantly lower than the 30% shown in the Figure.

Figure 18: Nuclear Power Capacity Scenarios for Estimation of Spent Fuel Production (10 MW) The assumed annual average capacity factors for the reactor fleets under the four different spent fuel scenarios are as shown in Figure 19, below. In Scenario 1, to approximate the previous energy basic plan (2010), the average capacity factor is assumed to increase to 90% in 2030. In the other scenarios, capacity factors decreases to 10% in 2012, consistent with actual experience post-Fukushima, then increase to reach 80% in 2015, maintaining that level until 2030. In reality, the actual capacity factor in 2013 was significantly lower than the 30% shown in the Figure.

Figure 19: Capacity Factor Assumptions for Nuclear Power under all Four Spent Fuel Scenarios

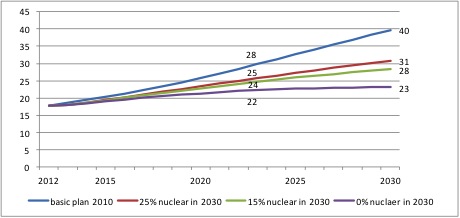

Based on the capacity and capacity factor assumptions as described above, electricity generation from nuclear power under the four spent fuel scenarios is calculated as shown in Figure 20, below. Electricity generated in 2011 FY was 1108 TWh. Assuming the level will be kept, nuclear ratio will reach about 50% in Scenario 1 (2030).

Figure 20: Electricity Generation from Nuclear Power in Four Spent Fuel Scenarios (TWh)

Accumulated Quantities of Spent Nuclear Fuel

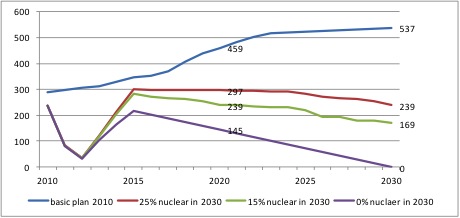

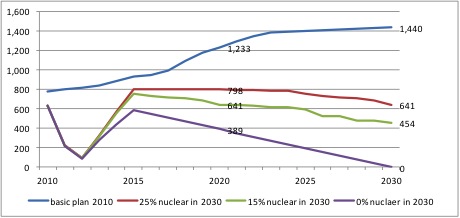

The total accumulated amount of spent fuel in Japan, including spent fuel in store on-site at power plants site storage and at the Rokkasho reprocessing plant as of April 2013 was about 17,770 tHM (tonnes of heavy metal) That is, 14,200+120+(3,362-20)=17662. According to the Atomic Energy Commission of Japan, the spent fuel stockpile located at the generation plants sites as of September 2011 was 14,200 tHM[11]. According to JNFL (Japan Nuclear Fuel Limited), which operates the reprocessing plant at Rokkasho, the accumulated received spent fuel in April 2013 amounts for 3,362 tHM[12]. Nuclear power generation between September 2011 and March 2013 amounted to 44.658 TWh, which would have produce about another 120 tHM of spent fuel, with newly discharged spent fuel received into storage during the fiscal year 2012 (April 2012 through March 2013) is about 20 tHM. Based on estimates of future annual spent fuel generation and the initial amounts in storage as of the end of 2012, the total spent fuel generated and accumulated can be calculated. A burn-up factor of 2.684 tHM/TWh is used to calculated spent fuel generation from nuclear power generation. Figure 21 shows annual spent fuel generation under each of the four spent fuel scenarios.  Figure 21: Annual Spent Fuel Generation in Japan under Four Scenarios (tHM/year) Based on these calculations, as shown in Figure 22, the accumulated spent fuel in Japan will be will be 40,000 tHM in Scenario1 by 2030, but will be much less in the other three scenarios. Even with nuclear phase out by 2030 (Scenario 4), however, the accumulated spent fuel will total 23,000 tHM in 2030.

Figure 21: Annual Spent Fuel Generation in Japan under Four Scenarios (tHM/year) Based on these calculations, as shown in Figure 22, the accumulated spent fuel in Japan will be will be 40,000 tHM in Scenario1 by 2030, but will be much less in the other three scenarios. Even with nuclear phase out by 2030 (Scenario 4), however, the accumulated spent fuel will total 23,000 tHM in 2030.

Figure 22: Accumulated spent fuel in Japan (103 tHM)

Spent Fuel Management Scenarios

Three paths for future spent fuel management in Japan were developed by the Japan Team.

- A. Reprocessing with re-use of reprocessed plutonium in mixed-oxide fuel (spent MOX fuel is disposed of, not reprocessed)

- A-2. Reprocessing with re-use of reprocessed plutonium in mixed-oxide fuel (spent MOX fuel is reprocessed)

- B. Direct disposal of all spent fuel

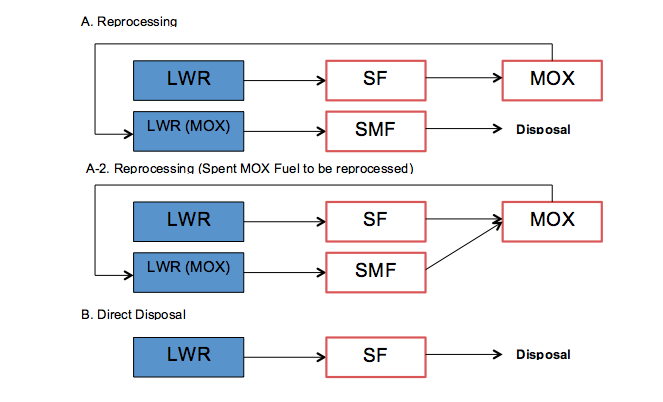

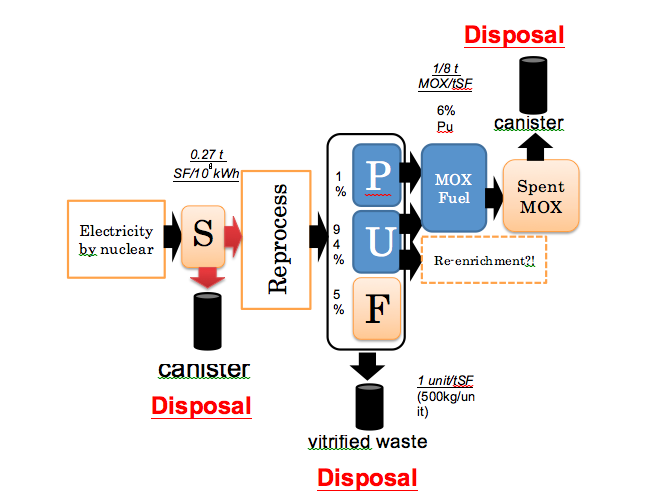

These three paths are shown schematically in Figure 23.  Figure 23: Three Paths of Future Spent Fuel Management in Japan Figure 23, below, shows a flow chart to indicate how the spent fuel will be processed. Nuclear power generation will produce spent fuel at a rate of 0.27 tHM spent fuel per 108 kWh. In the “B” path, spent fuel will be directly disposed of. When the spent fuel is to be reprocessed, the chemical structure of the spent fuel (Pu 1%, U 94%, fissile Products 5%) dictates the amount of plutonium produced, as well as the amount of vitrified waste exiting the process. 1 ton of spent fuel will produce 50 kg of high-level fission products, which will be disposed of in the form of vitrified canisters. 1 ton of spent fuel will produce 1 unit (500kg) of high-level vitrified waste. Plutonium and uranium separated from spent fuel will be mixed to produce MOX fuel for use in light water reactors. Plutonium will be enriched to account for 6% of the mass of MOX fuel, the rest of which will be uranium. 1 ton of spent fuel will produce 1/8 ton of MOX fuel. In Figure 24, the large “P” is plutonium, “U” is uranium, and “F” is fission products.

Figure 23: Three Paths of Future Spent Fuel Management in Japan Figure 23, below, shows a flow chart to indicate how the spent fuel will be processed. Nuclear power generation will produce spent fuel at a rate of 0.27 tHM spent fuel per 108 kWh. In the “B” path, spent fuel will be directly disposed of. When the spent fuel is to be reprocessed, the chemical structure of the spent fuel (Pu 1%, U 94%, fissile Products 5%) dictates the amount of plutonium produced, as well as the amount of vitrified waste exiting the process. 1 ton of spent fuel will produce 50 kg of high-level fission products, which will be disposed of in the form of vitrified canisters. 1 ton of spent fuel will produce 1 unit (500kg) of high-level vitrified waste. Plutonium and uranium separated from spent fuel will be mixed to produce MOX fuel for use in light water reactors. Plutonium will be enriched to account for 6% of the mass of MOX fuel, the rest of which will be uranium. 1 ton of spent fuel will produce 1/8 ton of MOX fuel. In Figure 24, the large “P” is plutonium, “U” is uranium, and “F” is fission products.  Figure 24: Assumptions for the processes

Figure 24: Assumptions for the processes

Pluthermal in Japan

The pluthermal concept involves the use of reprocessed plutonium in MOX fuel in conventional light water reactors, sometimes in combination with standard fuel elements using enriched uranium. Pluthermal power production is considered a means to stretch uranium resources, and a “bridge” to a future in which plutonium is produced and used in fast neutron reactors. A history of the pluthermal process in Japan is provided below. During the late 1980s and early 1990s, proving tests were done at the Mihama and Tsuruga nuclear power plants of the “pluthermal” concept,. A timeline of pluthermal-related In the “Long-term Nuclear plan” published in 1994, commercial operation of pluthermal plants in the late 1990s was planned, and the Nuclear Safety Commission reviewed the safety of the MOX fuel during 1990-1995. In 1997, given cabinet approval to suggest earliest implementation of pluthermal plants, electric utilities published their plans to implement pluthermal in 16-18 nuclear power reactors by 2015. In August 1999, the Ohma power plants, which were to be MOX-ABWR (advanced boiling water reactor)-type plants, which were designed to use fully MOX fuel, were added to the list of the new nuclear plants to be built in governments electric capacity development plan[13]. Since the pluthermal plan was published, however, there have been many incidents that have caused the implementation of pluthermal to be delayed. In 1999, falsification of MOX fuel data by BNFL occurred. In 2001, a local referendum in Kariwa, Nigata (close to Kashiwazaki-Kariwa) requested that the local nuclear plant not use pluthermal fueling[14]. Then, in 2002, TEPCO was found to have done voluntary inspection of pluthermal-related facilities inappropriately. Following these setbacks, many efforts to increase the public acceptance were carried out by the Japanese government and the electric utilities operating nuclear plants. In December of 2003, the Federation of Electric Power Companies (FEPC) reconfirmed that pluthermal would be start to be used in selected reactors where possible, with a target of using pluthermal in 16 to 18 reactors plants by 2015. In May 2009, three electric utilities (Chubu Electric, Shikoku Electric, and Kyushu Electric) finished MOX fuel transportation arrangements, and also several other electric utilities agreed to contracts with fuel processing companies, or approached local municipalities for permission to use MOX fuel in reactors. In April 2009, Japan Nuclear Fuel Ltd. (JNFL) changed the planned start date of their MOX fuel processing plant. In June 12th, 2009, FEPC reviewed its pluthermal plan, but reconfirmed the target of starting 16-18 pluthermal units by the 2015 fiscal year, when JNFL (Japan Nuclear Fuel Limited) was to have started pluthermal fuel fabrication operations. As a result, 3 pluthermal nuclear power units have started using MOX fuel. These are Genkai #3, operated by Kyushu Electric, in December, 2009; Ikata #3, operated by Shikoku Electric, in March, 2010; and Fukushima Daiichi #3, operated by TEPCO, in January, 2011 (two months before the Fukushima accident).

Scenarios for “Back-end” Spent Fuel Management: Direct Disposal/Reprocessing of Uranium Spent Fuel, and for MOX Fuel Reprocessing

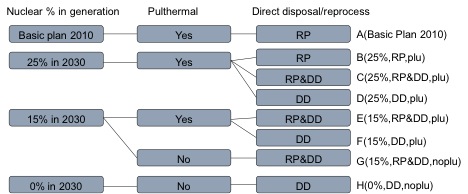

The Japan team established seven scenarios for Japan’s future activities in the areas of direct disposal of spent fuel, reprocessing of enriched uranium-based spent fuel, and reprocessing of MOX fuel, based on the combination of whether reprocessing or directly disposal or both were to be pursued, and on the target percentage of generation made up by nuclear power. Scenarios A through F include pluthermal nuclear power to consume MOX fuel, so that there will be less clean MOX fuel in Japan’s inventory, and thus less of a nuclear weapons proliferation risk, since it is relatively straightforward to separate plutonium from clean (fresh, or not yet irradiated) MOX fuel. Table 6 and Figure 26 show the assumptions used in these scenarios.

Table 6: Seven Scenarios of Nuclear Spent Fuel Management with Combinations of Reprocessing Policies, Nuclear Generation Targets, and Goals for Pluthermal Generation in Japan

|

1. Basic Plan |

2. 25% in 2030 |

3. 15% in 2030 |

3-B. 15% without Pluthermal |

4. 0% in 2030 ,without Pluthermal |

|

| RP (100% reprocessed) |

A |

B |

|||

| RP&DD (Half reprocessed, half to direct disposal) |

C |

E |

G |

||

| DD (100% direct disposal) |

D |

F |

H |

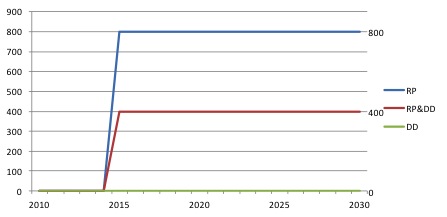

Figure 25: Back-end Spent Fuel Management Scenarios A-H, and Their Features Based on the back-end scenarios above we calculated: 1) the amount of spent fuel produced, and 2) the amount of MOX fuel (which is equal to the amount of spent MOX fuel). As we described above, the amount of MOX fuel and spent MOX fuel is 1/8 ton per ton of original spent fuel. Plants configured to use MOX fuel (pluthermal nuclear power plants) are identified as shown in Table 6, below, according to the FEPC (Federation of Electric Power Companies) plan as described in 2009[15]. In the plan, utilities planned to operate 16-18 pluthermal power plants by the 2015 fiscal year. We assumed that an additional 12 plants will start operating in 2015, in addition to the three plants that have already started pluthermal generation, but excluding the damaged and inoperable Fukushima Daiichi unit #3. The total capacity of these plants over time is shown in Figure 25. (It should be noted that as of this writing, at the end of 2013, it appears that 2015 might be too early for an additional 12 plants to realistically start operating using MOX fuel, if indeed they operate at all. As of the time of the writing of this report (December 2013), no nuclear power plants were operating.) The 100% reprocessing scenario (RP) assumes full operation of the Rokkasho reprocessing plant. In that scenario, in which 100% of spent fuel from light water reactors is sent to reprocessing, 800 tHM of spent fuel will be reprocessed to MOX fuel annually starting from 2015, resulting in a decrease in Japan’s spent fuel stockpile. In the half reprocessing/half direct disposal (denoted as RP&DD) scenarios, 400 tHM of spent fuel will be reprocessed each year after 2015. In the DD scenarios, spent fuel will not be reprocessed to MOX fuel, but will be disposed of directly,. Direct disposal requires sites in which canisters of spent fuel and other nuclear wastes can be buried (or stored over the very long term). In scenarios including DD and RP&DD elements, we assume construction of a final disposal site will start in 2015, and start operating in 2035, so that there will be no influence on the amount of spent fuel stockpiled above ground before 2035.

Figure 25: Back-end Spent Fuel Management Scenarios A-H, and Their Features Based on the back-end scenarios above we calculated: 1) the amount of spent fuel produced, and 2) the amount of MOX fuel (which is equal to the amount of spent MOX fuel). As we described above, the amount of MOX fuel and spent MOX fuel is 1/8 ton per ton of original spent fuel. Plants configured to use MOX fuel (pluthermal nuclear power plants) are identified as shown in Table 6, below, according to the FEPC (Federation of Electric Power Companies) plan as described in 2009[15]. In the plan, utilities planned to operate 16-18 pluthermal power plants by the 2015 fiscal year. We assumed that an additional 12 plants will start operating in 2015, in addition to the three plants that have already started pluthermal generation, but excluding the damaged and inoperable Fukushima Daiichi unit #3. The total capacity of these plants over time is shown in Figure 25. (It should be noted that as of this writing, at the end of 2013, it appears that 2015 might be too early for an additional 12 plants to realistically start operating using MOX fuel, if indeed they operate at all. As of the time of the writing of this report (December 2013), no nuclear power plants were operating.) The 100% reprocessing scenario (RP) assumes full operation of the Rokkasho reprocessing plant. In that scenario, in which 100% of spent fuel from light water reactors is sent to reprocessing, 800 tHM of spent fuel will be reprocessed to MOX fuel annually starting from 2015, resulting in a decrease in Japan’s spent fuel stockpile. In the half reprocessing/half direct disposal (denoted as RP&DD) scenarios, 400 tHM of spent fuel will be reprocessed each year after 2015. In the DD scenarios, spent fuel will not be reprocessed to MOX fuel, but will be disposed of directly,. Direct disposal requires sites in which canisters of spent fuel and other nuclear wastes can be buried (or stored over the very long term). In scenarios including DD and RP&DD elements, we assume construction of a final disposal site will start in 2015, and start operating in 2035, so that there will be no influence on the amount of spent fuel stockpiled above ground before 2035.

Table 7: List of Potential Pluthermal Power Plants

|

Electric utility |

# of plants |

# of plants in FEPC plan |

Specified plant |

capacity (MW) |

current status |

Start year |

Max. mix ratio |

| Hokkaido |

1 |

1 |

Tomari #3 |

912 |

Planning |

2015* |

30% |

| Tohoku |

1 |

1 |

Onagawa #3 |

825 |

Planning |

2015* |

30% |

| TEPCO |

1 |

3~4 |

Kashiwazaki-kariwa #3 |

1100 |

planning |

2015* |

30% |

| Chubu |

1 |

1 |

Hamaoka #4 |

1137 |

Planning |

2015* |

30% |

| Hokuriku |

1 |

1 |

Shika #2 |

1206 |

Planning |

2015* |

30% |

| Kansai |

4 |

3~4 |

Takahama #3 |

870 |

under operation |

2010 |

30% |

| Takahama #4 |

870 |

Planning |

2015* |

30% |

|||

| Ohi #1 |

1175 |

Planning |

2015* |

30% |

|||

| Ohi #2 |

1175 |

Planning |

2015* |

30% |

|||

| Chugoku |

1 |

1 |

Shimane #2 |

820 |

Planning |

2015* |

30% |

| Shikoku |

1 |

1 |

Ikata #3 |

890 |

under operation |

2010 |

30% |

| Kyushu |

1 |

1 |

Genkai #3 |

1180 |

under operation |

2009 |

30% |

| JAPC |

2 |

2 |

Tokai Daini |

1100 |

Planning |

2015* |

30% |

| Tsuruga #2 |

1160 |

Planning |

2015* |

30% |

|||

| J-Power |

1 |

1 |

Ohma |

1383 |

Planning |

2015* |

100% |

| Total |

15 |

16~18 |

|||||

Note: The Fukushima Daiichi #3 plant started pluthermal operation in October, 2010. A decision was made to decommission this unit after the Fukushima accident following the Sendai earthquake on March 11th, 2011, so this plant is excluded from the list. * Scenario assumption.

Figure 26: Capacity of Pluthermal Power Plants (GW)

The fraction of the reactor cores made up of MOX fuel in each plutthermal reactor was assigned as shown Table 7. The Ohma power plant is designed to use 100% MOX fuel, but the other plants where MOX fuel is to be used were originally designed for enriched uranium fuel, and are thus assumed to have a maximum fraction of MOX in their cores of 30%. Also, it is assumed that mixture ratio for the pluthermal reactors other than Ohma is 10% MOX for the first year of operation with MOX fuel. The per-unit enriched uranium and MOX fuel use in pluthermal plants is assumed to be 2.684 tHM/TWh produced, with the same mass of spent MOX fuel produced per TWh of electricity as the fuel input. In the scenarios that assume MOX fuel will be used in pluthermal plants, 107-121 tHM of MOX fuel will be used annually, with production of an equivalent amount of spent MOX fuel each year, as shown in Figure 27.

Figure 27: Annual MOX Fuel Used (and spent MOX fuel produced) in Pluthermal Plants in Scenarios A-F (tHM/year)

Result of Scenario Study

Based on the inputs and assumptions above, the amounts of spent fuel, directly disposed spent fuel, separated plutonium in MOX fuel, and spent MOX fuel were calculated. The annual production and cumulative total spent fuel produced are shown in Figure 28 and Figure 30, respectively, for the various back-end scenarios, while Figure 29 shows the annual amount of spent fuel reprocessed.

Spent Fuel Production and Accumulation

Under all of the back-end fuel cycle scenarios explored, spent fuel is produced in proportion to the electricity production from nuclear power plants. Spent fuel is reprocessed in the RP and RP&DD scenario branches, which reduces the amount of spent fuel accumulated, relative to branches without reprocessing, though under all of the scenarios explored 2030 spent fuel inventories are higher than inventories as they stood in 2012. The amount of accumulated spent fuel would be 27 thousand tons of HM in 2030 in the case where Japan was assumed to follow the previous energy basic plan starting from 2010 (Scenario A). If the fraction of electricity generation supplied by nuclear power in surpasses 15%, and reprocessing is not used in the future, the amount of spent fuel accumulated by 2030 will somewhat exceed the total in scenario A. By 2030, accumulated spent fuel is about 28,000 and 30,000 tHM in scenarios D and F, respectively. If the reprocessing plant (Rokkasho plant) successfully starts commercial operation in 2015, the spent fuel stockpile by 2030 will be less than in scenario A in all other scenarios (Scenario B, C, E, G, and H).

Figure 28: Annual spent fuel production (tHM/year)

Figure 29: Annual reprocessed amount (tHM/year)

Figure 30: Accumulated “spent fuel” (not including spent MOX fuel)

MOX Fuel Stockpiles

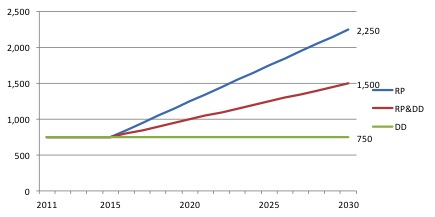

MOX fuels are produced primarily at the reprocessing plant in Rokkasho. In the RP scenarios, 800 tHM of spent fuel will be reprocessed annually[16] to produce 800*1/8 tHM of MOX fuel. In RP&DD scenarios, 400 tHM of spent fuel will be reprocessed annually to produce 400*1/8 tHM of MOX fuel. Figure 31 shows the cumulative MOX fuel projection in the various types of back-end scenarios.

Figure 31: Accumulated MOX Fuel Produced (tHM of MOX fuel)

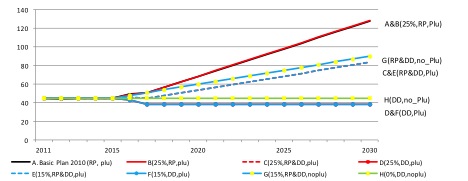

Figure 32 shows the amount of accumulated plutonium in MOX fuel in Japan under the different back-end fuel cycle scenarios considered. The accumulated amount of plutonium in MOX fuel will not increase from the initial value of 45 tons in 2011 in scenario H, which assumes no reprocessing, and no use of pluthermal fueling in reactors. In the scenario D and F, where no reprocessing is operating but in which it is assumed that pluthermal power plants will operate, the amount of plutonium in accumulated MOX fuel will decrease slightly over time, to 39 tons in 2030. In scenarios A and B, even though there will be pluthermal plants operating, the amount of plutonium in MOX fuel will increase to reach almost 130 tons in 2030. In Scenario G, where the reprocessing plants operates at half of its capacity, but there is no use of pluthermal power production, the amount of plutonium in MOX fuel will increase to reach 90 tons of plutonium in 2030. If pluthermal power operates, the plutonium stockpile will decrease by 6 tons of plutonium (equivalent to 107 tHM of MOX fuel) to reach 84 tons of plutonium in 2030. Scenarios D and F, focusing on direct disposal, result in the smallest plutonium stockpiles by 2030 among all of the scenarios. Scenarios D and F assume no reprocessing, but with pluthermal operation. In scenarios D and F, the resulting plutonium in MOX fuel by 2030 is slightly lower than in Japan’s current MOX fuel inventory (2011-2014).

Figure 32: Accumulated MOX Fuel Considering Usage in Pluthermal Plants (tons of plutonium in MOX fuel)

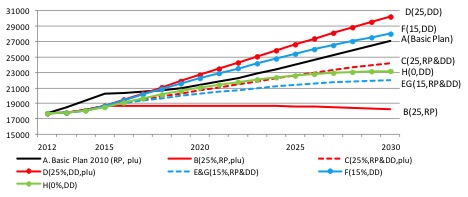

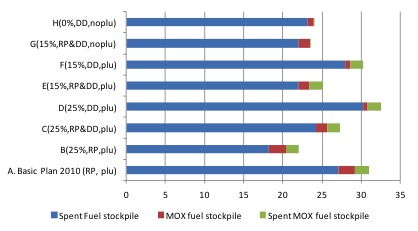

Figure 33 compares the estimated year 2030 stockpiles of spent fuel, spent MOX fuel, and fresh MOX fuel under the back-end fuel cycle scenarios evaluated. These results indicate that a reprocessing capacity of 800 tHM/year is not sufficient to decrease spent fuel stockpiles in Japan. Moreover, the existing MOX fuel stockpile, which contains plutonium separated from spent fuel, will remain quite large amount in all scenarios that assumes reprocessing. On the other hand, the amount of spent MOX fuel will not be that large, even assuming the current plans for pluthermal capacity of 15 plants (of which 14 plants can use a core containing nom more than 30% MOX). This is of significance because spent MOX fuel requires different handling than spent enriched uranium fuel because of its different radiological properties.  Figure 33: Accumulated Spent (enriched uranium) Fuel, MOX fuel, and Spent MOX fuel in 2030 (103 tHM)

Figure 33: Accumulated Spent (enriched uranium) Fuel, MOX fuel, and Spent MOX fuel in 2030 (103 tHM)

II. CONCLUSION

After the Great East Japan (Sendai) Earthquake and the Fukushima nuclear accident, most Japanese conservative policymakers changed their public stance from “reluctant toward renewables, positive toward nuclear”, to “positive toward both renewable and nuclear” or “positive toward renewables, negative to nuclear.” It is an interesting indicator of the profound impact of the Fukushima accident on the Japanese public psyche that politicians such as former Prime Minister Koizumi are now supporting a “no nuclear”, or no further nuclear, energy future for Japan, given their strong support for nuclear power in the past. Feed-in tariff started for all renewable sources of electricity in July, 2012. The tariff rates are set high enough to encourage many kinds of companies, from small to large, to enter the renewable power business. Since it has been only less than 2 years since the FIT started, the majority of newly operating renewable power plants are photovoltaic systems, because other types of renewable electricity sources require longer lead times for development and installation before they begin generating power. There are, however, many projects going on for other sources of renewable electricity, and if the Japanese government does its best to deploy renewables in the way that current policies direct, Japan can overcome deployment issues and reach a future in which a large percentage of the electricity used in Japan is generated from renewable resources. Apart from the recent increase in renewable energy deployment, how Japan’s power sector will evolve is at the moment very unclear, and depends substantially on how the government chooses to move forward, or not, with the nuclear power sector. Under the previous government, an agreement was reach to essentially phase out nuclear power within 20 years or so. This policy is being revisited under the Abe government, and it is possible that the existing nuclear reactors, all of which are currently off-line (or, in the case of units 1-4 of Fukushima Daiichi, damaged beyond repair), will eventually be brought back on line. The three nuclear capacity deployment scenarios described in this paper show very divergent results—in particular between the “Maximum Nuclear” and both the Reference and “Minimum Nuclear” cases, and also have different implications for the requirements for fossil fuels and, relatedly, for greenhouse gas emissions from the power sector. Also uncertain at present is Japan’s policies for pluthermal power plants, that is, using mixed-oxide fuel in light water reactors to help to reduce the inventory of plutonium-bearing, but non-irradiated, MOX fuel that Japan has built up through its domestic reprocessing activities and through reprocessing done under contract for Japanese utilities in Europe under . Based on the analysis described above, however, the use of pluthermal reactors will have at best relatively little impact on the current inventory of plutonium-bearing MOX fuel, and at worst could substantially increase the inventory of MOX fuel. The use of MOX fuel in pluthermal reactors will also have relatively little impact on Japan’s inventory of spent fuel, in scenarios with or without reprocessing. Overall, it seems clear that reprocessing and the use of MOX fuel in pluthermal reactors will do little to address Japan’s spent nuclear fuel problem, which therefore will have to be addressed through other means that will necessarily incorporate both political and technical dimensions. Meanwhile, questions abound regarding Japan’s future energy policy. How will Japan meet its GHG emissions targets, even factoring in declining population and a slow economy? Can meeting those targets be done without substantially restarting the nuclear sector? Will electricity sector restructuring actually come to fruition, how can a restructured Japanese electricity system be regulated so that public goal, such as GHG emissions targets, are salient to the planning process, and what will happen to the current electricity sector “players” if the sector is effectively deregulated? Will policies be kept in place to make sure that the post-Fukushima momentum for renewable energy deployment is maintained? All of these questions are crucial, but all have yet to be answered as of this unsettled moment in Japan’s energy policy.